Research · Cycle Sequencing & Phases

AI Is Rewriting Software Business Models

AI and Software: The Mechanism Behind the Repricing

This note translates a recent software selloff into Our Strategy framework: mechanisms over narratives, signals over outcomes, sequencing over timing, and probabilities over conviction.

The core claim is not that “software is dead.” The claim is that artificial intelligence changes substitution risk for specific software business models, and markets are repricing that risk unevenly.

When the market sells a sector in a clustered way, we first ask a plumbing question: is this a liquidity event, a credit event, a positioning unwind, or a fundamentals reclassification.

In this case, the dominant mechanism looks like a fundamentals reclassification accelerated by narrative intensity: investors are separating software into infrastructure-like durability versus workflow-like replaceability.

Our Strategy Frame

Where this fits in the phase model

We treat the current software episode as a late-cycle multiple compression and rotation problem rather than a clean “risk-on or risk-off” call. In our sequencing language, this sits most naturally in

Phase Two pressure: valuations can compress even if revenues are still growing, because the market is repricing durability and switching costs.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Phase pressure, probabilities, and time windows

These are probability windows, not forecasts. They are designed to remain useful even if the exact path differs.

-

Current phase continuation: We assign a sixty to seventy percent probability that multiple compression and business-model sorting remains the dominant force

through June twenty twenty-six, especially for per-user software exposed to seat compression. -

Next phase transition: We assign a twenty to thirty percent probability that this evolves into a sharper reset by December twenty twenty-six

if earnings expectations fail to adjust to substitution and pricing pressure. -

Plus two phases: We assign a fifteen to twenty five percent probability of a broader forced-liquidity window by June twenty twenty-seven

if credit spreads widen materially and funding conditions tighten, temporarily pushing correlations higher across risk assets. -

Stabilization path: We assign a forty to fifty percent probability that by December twenty twenty-seven the market has largely completed

a first pass at reclassification and leadership becomes more dispersion-driven, with durable platforms regaining relative strength.

The Core Mechanism: Substitution Risk Meets Revenue Model Math

Seat compression

Many software platforms monetize through per-user pricing. If artificial intelligence allows one worker to produce the output of multiple workers, the buyer can reduce seats.

That is “seat compression,” and it is a structural headwind for revenue models tied to headcount rather than outcomes.

Workflow automation vulnerability

The highest vulnerability sits in software whose value proposition is primarily workflow automation and whose workflow can be described in natural language.

As large language models and agentic systems improve, they become substitutes for point solutions that are easy to replicate or bundle.

Durability filters

Our Strategy uses three durability filters that tend to separate “survivors” from “replaceables” in technology reclassifications:

- Physical execution: businesses tied to scarce physical infrastructure, such as cloud compute, networks, and data centers.

- Regulatory entrenchment: systems embedded in regulated environments where switching risk is high and auditability matters.

- Deep integration: platforms so embedded in operations that replacement costs exceed expected savings.

Second-order beneficiaries

Artificial intelligence scaling tends to increase demand for infrastructure and control layers: compute, storage, networking, observability, and cybersecurity.

In Our Strategy language, these behave more like picks-and-shovels exposures than discretionary workflow tools.

What Changes vs What Does Not Change

What changes

- Valuation logic shifts: the market increasingly prices durability, switching costs, and integration moats over pure growth narratives.

- Pricing power is tested: buyers compare subscription costs to agentic alternatives and negotiate harder.

- Sales motions adjust: procurement cycles can lengthen as enterprise buyers evaluate AI substitution and bundling risk.

- Winners become infrastructure-like: revenue tied to compute, networks, security, and data becomes more structurally advantaged as AI scales.

What does not change

- Markets reprice in sequences: early moves are often narrative-amplified, later moves depend on earnings and credit conditions.

- Liquidity still dominates extremes: if funding stress arrives, correlations can rise and “good businesses” can sell off temporarily.

- Optionality remains an asset: Our Strategy does not require full commitment to any single narrative, only disciplined sequencing.

Signals We Monitor: Confirmations vs Invalidations

Confirmations

- Seat metrics deteriorate: net adds, retention, and per-seat pricing weaken in per-user models.

- Contract language shifts: more outcome-based pricing, usage-based pricing, or renegotiations tied to AI productivity.

- Infrastructure demand persists: cloud and network utilization grows alongside AI adoption.

- Security spend remains resilient: security budgets hold or rise as attack surface expands.

Invalidations

- Incumbents absorb AI and defend pricing: threatened platforms successfully bundle AI while preserving economics.

- Switching costs prove higher than assumed: buyers avoid substitution due to operational or compliance risk.

- AI substitution stalls: agentic tools fail reliability or governance thresholds at enterprise scale.

Monitoring List (Observation Only)

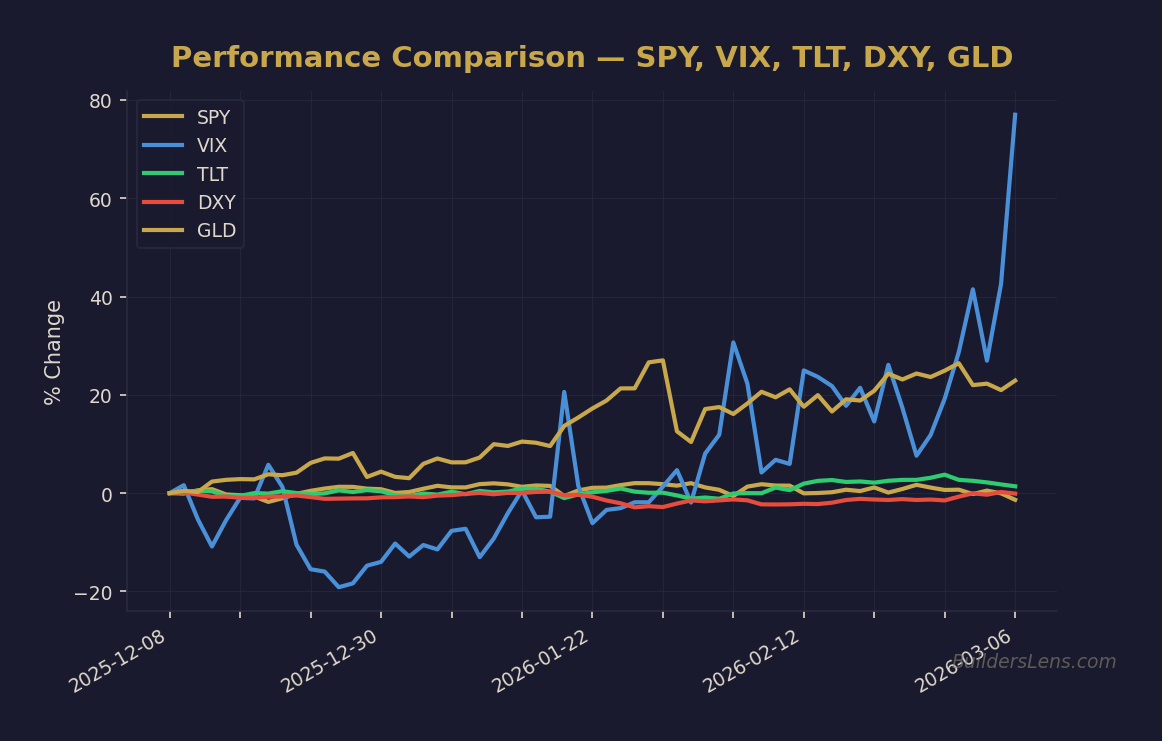

- Broad risk: SPY, VIX

- Long duration: TLT, ZROZ

- AI and semis beta: SMH, AIQ, CHAT

- Dollar and global sensitivity: EEM

- Hard assets context: Gold, Silver, Oil, Copper

Discipline

Our Strategy remains mechanism-led and conditional. We observe signals, assign probabilities, and sequence exposure accordingly.

Educational only. This is not investment advice.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.