Research · Uncategorized

Asset Inflation or Late-Cycle Compression? Mapping the Signal

Our Strategy: Translating the Two-Tier Economy Narrative Into Signals

In Our Strategy, we do not predict headlines. We translate claims into

signal buckets, map mechanisms, and express

the cycle as phase pressure with probabilities.

The goal is educational: improve signal versus noise discrimination,

clarify sequencing, and preserve optionality.

This is not financial advice.

The source video argues that America is entering a structural wealth

transfer regime driven by persistent deficits, policy support, and

asset inflation, alongside visible strain in lower-income consumption.

Our task is to separate what is structural from what is cyclical,

and what is narrative from what is confirmable.

What the Video Is Claiming

The central claims can be summarized as follows:

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

- Two-tier economy: Higher-income households remain resilient while lower-income households experience strain.

- Policy support: Liquidity injections and rate suppression may extend asset prices.

- Persistent deficits: Higher issuance potentially leads to monetization dynamics.

- Housing pressure: Affordability constraints meet supply limitations and rising construction costs.

- Wealth concentration: Asset owners benefit earlier in liquidity-driven cycles.

Our Strategy does not accept or reject this as a story.

We translate it into signals and ask:

What confirms it?

What invalidates it?

And what phase sequencing does it imply?

Signal Classification

Labor and Consumption

Income distribution affects spending resilience.

Spending affects earnings durability.

Labor deterioration becomes critical when weakness broadens

beyond isolated income segments.

Credit and Refinancing

Housing links household balance sheets, mortgage markets,

and bank collateral structures.

If refinancing channels remain open, stress can be delayed.

If refinancing tightens, phase pressure rises quickly.

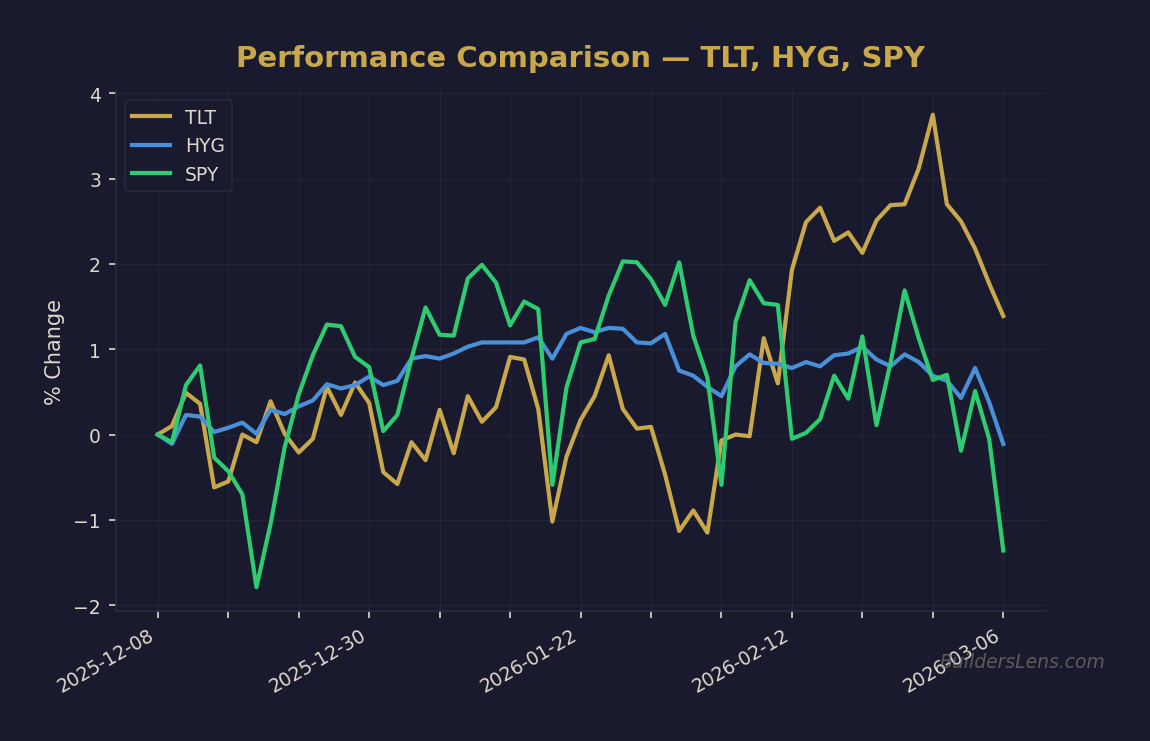

Yield Direction

The direction of long-term yields matters more than the curve shape.

If long yields remain elevated despite policy easing,

valuation compression becomes more likely.

Liquidity Plumbing

Liquidity operations support financial assets first.

Labor and credit stress often lag.

Funding conditions and auction demand are critical confirmation signals.

Mechanism: How the System Transmits

Step 1: Persistent deficits require continuous funding.

Step 2: If private demand weakens, policy tools absorb supply.

Step 3: Liquidity reaches financial assets before households.

Step 4: Labor and credit deterioration follow with delay.

Step 5: Housing becomes the pressure point linking policy and credit.

Policy can delay stress.

It cannot permanently override structural debt constraints.

Phase Mapping Within Our Five-Phase Framework

Current signals align most closely with late Phase 1 transitioning

toward Phase 2 pressure.

- Phase 1: Liquidity supportive, asset resilience persists.

- Phase 2: Valuation compression risk rises beneath surface stability.

- Phase 3 risk: Increases only if credit spreads widen persistently and labor deteriorates materially.

Probability Calibration

- Phase 1 continuation: 35% to 50%

- Phase 2 compression: 35% to 45%

- Phase 3 stress window: 15% to 25%

- Phase 4 forced liquidity tail risk: 5% to 15%

These are probability bands, not predictions.

Liquidity momentum, credit spreads, and yield direction

determine sequencing.

What Changes in Our Strategy

- Increase monitoring weight on housing and refinancing data.

- Tighten exit discipline during melt-up participation.

- Track long-end yields and Treasury auction quality closely.

- Maintain optionality as Phase 2 pressure rises.

What Does Not Change

- No all-in positioning based on narrative alone.

- No ideological bias toward any asset class.

- Cash remains strategic optionality.

- Confirmation remains required before elevating Phase 3 probabilities.

Invalidation Conditions

- Debt growth moderates without monetization pressure.

- Productivity offsets structural debt constraints.

- Housing clears supply through genuine price discovery.

- Credit spreads remain tight despite elevated issuance.

Closing Perspective

Policy delay is real.

Structural math is also real.

Our Strategy focuses on sequencing, confirmation,

and disciplined probability management.

We do not need to be early.

We simply cannot afford to be late.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.