Research · Credit & Liquidity

California Wealth Tax, Capital Flight, and Housing Stress

California Wealth Tax, Capital Flight, and Housing Stress

A Phase-Based Macro Analysis Through Our Strategy Framework

Strategy Anchor

In Our Strategy, we operate within a five phase macro framework built on probabilities, sequencing, and optionality.

We are not attempting to predict headlines or political outcomes. We are identifying transmission mechanisms.

The California wealth tax discussion is not primarily a political story. It is a capital flow, credit margin, and structural housing story.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

What Is Actually Being Argued

The central claim is that California’s proposed wealth tax, combined with rent freezes, rising insurance premiums, and high refinancing rates, is accelerating capital flight.

The argument suggests a sequence:

- Mobile capital relocates.

- Investment slows and small businesses weaken.

- Landlords experience margin compression.

- Distress probability increases.

- Institutional buyers re-enter at lower valuations.

The question for Our Strategy is not whether this narrative is emotionally compelling. The question is where it fits in the phase sequence.

Signal Classification

- Policy and Structural Distortion: Wealth tax proposals, mansion taxes, rent freezes.

- Credit Stress: Landlord margin compression and refinancing pressure.

- Yield Direction Risk: Low-rate loans resetting materially higher.

- Housing Transmission Channel: Insurance spikes, investor concentration, vacancy risk.

- Labor Spillover Risk: Business closures feeding employment weakness.

This is primarily a housing and credit compression story, not yet a confirmed liquidity plumbing event.

The Transmission Mechanism

Policy increases the marginal cost of capital within a state.

Mobile capital relocates. High net worth individuals and corporations can move.

Reduced capital base weakens investment and hiring.

Landlords face rising operating costs while rent growth may be constrained.

Refinancing pressure emerges as previously low-rate loans reset higher.

Cash flow compresses. Distress risk rises. Price discovery follows.

Markets can ignore this dynamic temporarily because national indices dilute state-level stress and policy tools can extend timelines.

Phase Mapping

This narrative reinforces rising Phase Two pressure.

Phase Two represents multiple compression under policy delay. Structural pressures build while surface stability persists.

Phase Three becomes probable only if housing stress transmits into labor deterioration and broader credit widening.

Current evidence suggests localized strain rather than confirmed systemic transition.

Probability and Timeline Assessment

Next 3 Months

- 55–65%: Continued localized housing compression.

- 25–35%: Regional correction accelerates.

- 5–15%: Disorderly spillover into broader credit markets.

Next 6 Months

- 40–50%: Structural compression masked by policy delay.

- 30–40%: Broader credit repricing tied to refinancing wall.

- 10–20%: Clear Phase Three transition nationally.

Next 12 Months

- Gradual reset with contained stress.

- Broader cyclical reset if labor and credit deteriorate together.

- Extended delay through further policy intervention.

The key variable is labor transmission. Housing stress without labor deterioration remains manageable. Housing stress plus labor weakness materially raises phase pressure.

What Changes in Our Strategy

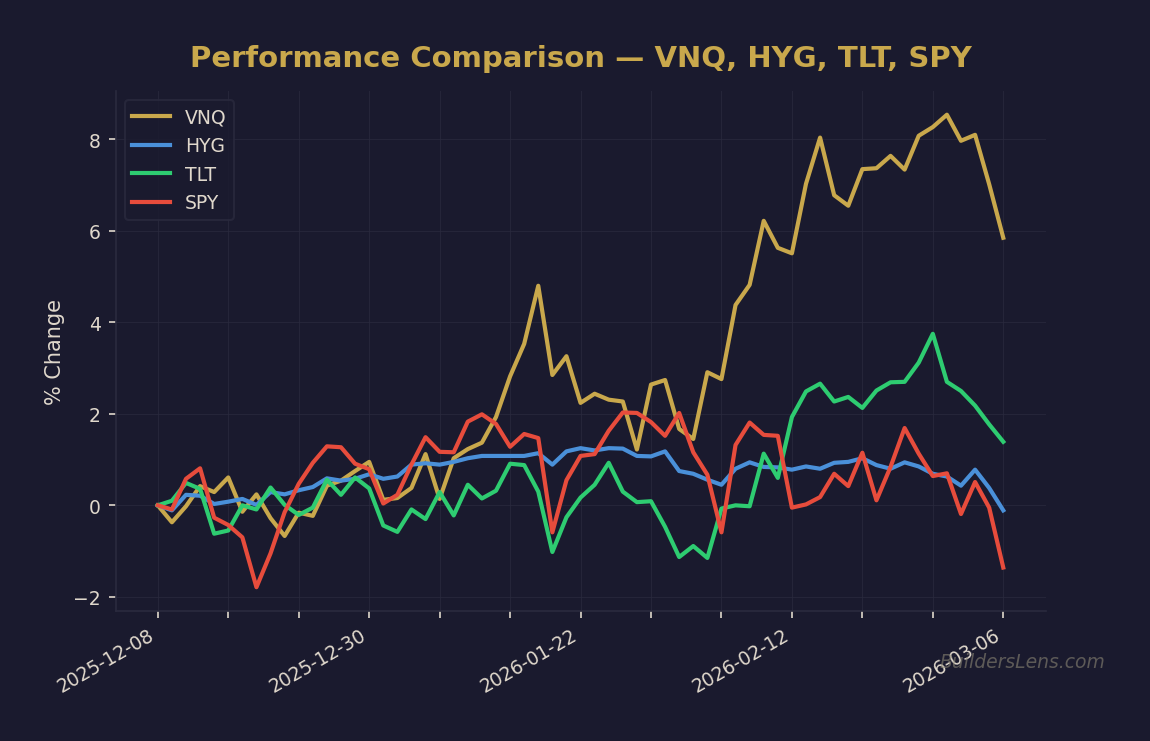

- Upgrade monitoring of housing stress metrics.

- Track regional bank exposure to commercial real estate.

- Monitor delinquency trends and high yield spreads.

- Maintain optionality for potential distress deployment.

What Does Not Change

- No confirmed systemic liquidity plumbing failure.

- No confirmed national labor collapse.

- No justification for premature crash ladder deployment.

- No abandonment of disciplined participation where signals allow.

Policy Delay Versus Structural Reset Overlay

This situation reflects the tension between policy delay and structural reset.

Policy delay can extend timelines and mask deterioration. It does not remove leverage constraints.

Phase Two environments often appear stable at the index level while volatility rises underneath.

Structural reset becomes dominant only when policy tools lose marginal effectiveness.

Action Checklist

- Mortgage delinquency acceleration.

- Lending standard tightening.

- High yield spread expansion.

- Labor weakness tied to business closures.

- Treasury yield behavior during stress episodes.

Invalidation Conditions

- Refinancing stress moderates materially.

- Credit spreads remain contained.

- Labor markets stabilize.

- Housing clears without forced liquidation.

Final Perspective

The California wealth tax narrative raises Phase Two pressure within a specific geography and sector.

It does not yet confirm systemic breakdown.

In Our Strategy, we survive melt ups, monitor compression, and deploy aggressively only when forced liquidity creates asymmetric opportunity.

We do not need to be early. We just cannot afford to be late.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.