Research · Credit & Liquidity

China can look “stable” on the surface while its credit engine is quietly breaking underneath.

Hook

China can look “stable” on the surface while its credit engine is quietly breaking underneath.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

In this episode, Our Strategy translates new China credit and banking data into a five-phase framework focused on credit transmission, policy constraints, and global spillover risk — not headlines.

Disclaimer

This post is for educational macro commentary only and is not financial advice. It reflects a probability-weighted macro framework and does not recommend specific trades.

Our Strategy Lens

Our Strategy prioritizes credit creation and funding mechanics because that’s where systemic stress forms first — often long before equity markets react.

China matters here not as a “growth engine,” but as a stress amplifier: when credit breaks, policy choices narrow, and spillovers show up through currencies, trade, and global risk appetite.

Signals That Matter

1) Household Credit Collapse (Not a Slowdown)

- Household borrowing rolls over hard when confidence breaks and property stops functioning as collateral

- Loan growth falling becomes a feedback loop: less credit → weaker activity → more caution → even less credit

In this framing, the key issue is not “weak demand” — it’s the failure of the credit transmission mechanism.

2) “Recapitalization” Was Containment, Not Stimulus

- Bank support can prevent an immediate cascade without restarting lending

- Impaired banks protect capital first and restrict risk second

- Lower rates can worsen the problem by compressing bank margins and weakening the incentive to expand credit

That’s why policy easing can look active while the real economy remains credit-starved.

3) Property Stress Becomes System Stress (Vanke as the Signal)

- Property drives confidence, collateral values, and willingness to borrow

- When a “safe” name shows stress, it signals the system is moving from “rescue” to containment

- Refinancing friction tightens the loop: developers struggle → banks pull back → credit shrinks further

This is how a property problem becomes a banking and credit creation problem.

4) Ultra-Low Bond Yields Signal Deflation Risk (Not Recovery)

- Very low yields can reflect low growth expectations and deflation pressure

- They can also reflect a system seeking safety because it can’t expand risk in the private sector

In Our Strategy terms: low yields here are less “bullish” and more diagnostic.

5) The Yuan Rising for the “Wrong” Reason

- A currency can stabilize because of trade flows and controls, not because credit conditions improved

- Trade dollars can support funding without restoring domestic credit creation

The difference matters: stability from exports does not equal a repaired credit system.

Phase Mapping (Our Strategy Framework)

| Phase | Definition | Status | Key Signal |

|---|---|---|---|

| Phase 1 | Hidden Fragility | Past / replaced | Credit creation no longer responding to policy narratives |

| Phase 2 | Asymmetric Sensitivity | Active (global spillover watch) | FX stability masking stress; rising sensitivity to trade/flow slowdown |

| Phase 3 | Forced Repricing / Credit Breakdown | Showing internally (China) | Household credit collapse + impaired banks + property refinancing pressure |

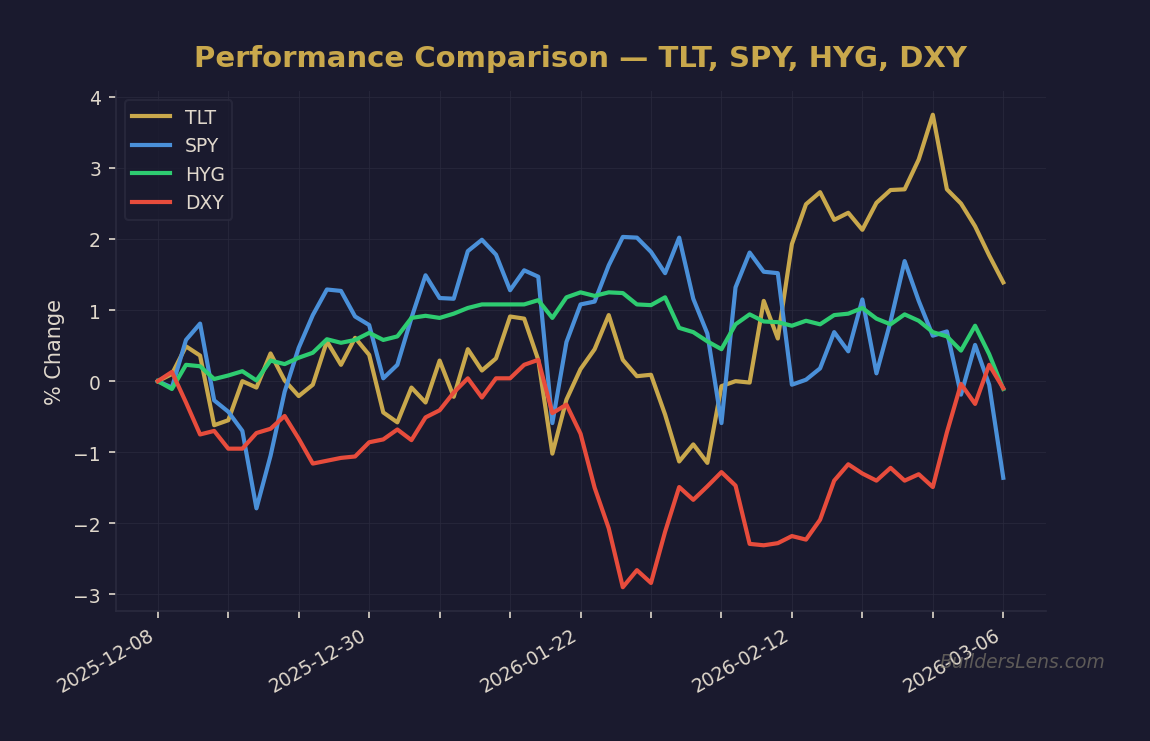

Sensitive Instruments to Monitor (Not Trade Calls)

- FX (CNH / USD and Asia FX complex) — funding and confidence transmission

- China / EM exposure — spillover sensitivity as growth expectations shift

- Industrial commodities — demand signal if China weakness transmits globally

- Global duration (TLT / long-end rates) — deflation vs term-premium regime interaction

- Broad risk (SPY) + liquidity proxies — if correlation rises, repricing risk increases

What Changed

- Credit data suggests deeper impairment than “slow growth” headlines imply

- Policy actions look more like containment than true stimulus transmission

- China’s role shifts further toward stress amplifier rather than stabilizer

What Didn’t Change

- No single China datapoint “times” a global equity top

- Trade flow strength can delay visible consequences

- Phase transitions still require confirmation across credit/funding signals, not narratives

Process Adjustments (Not Trade Recommendations)

- Move credit and FX signals higher in the stack when China credit breaks

- Respect spillover sequencing: FX → funding → credit → broader risk

- Preserve optionality when outcomes widen and correlation risk rises

- Track confirmation via spreads, funding stress, and cross-asset transmission

Original Source & Credit

This episode reviews and translates the following original video for educational purposes:

Original video — China credit / banking analysis

Close

China’s story isn’t “stimulus will fix it.” The story is whether a damaged credit system can restart without breaking banks — and whether exports can keep masking domestic weakness.

In late-cycle conditions, credit transmission matters more than headlines.

Background is generated via Prompt 2.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze TLT (Long-Term Treasuries)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.