Research · Credit & Liquidity

China’s Banks Are Already Inside the Trap

China’s Banking System: Margin Compression and Credit Constraint

Recent Chinese banking data reflects a structural balance sheet constraint rather than a conventional cyclical slowdown. Informal reductions in the People’s Bank of China medium-term lending facility rate have coincided with relatively sticky loan prime rates, signaling margin defense behavior among banks. When funding costs decline but lending rates do not fall proportionally, banks are protecting net interest spread. That behavior is inconsistent with aggressive credit expansion.

Simultaneously, regulators have expanded the list of domestically systemically important banks and intensified supervisory oversight. Official non-performing loan ratios remain stable on paper, yet regulatory tightening suggests underlying asset quality concerns. The divergence between reported stability and regulatory posture is a key signal.

Mechanism: Why Lower Rates May Not Stimulate

In systems with rising bad loan pressure, lower interest rates compress bank profitability. Profitability is the internal recapitalization mechanism that allows banks to absorb credit losses. When margins shrink, the incentive to expand new lending declines. This creates a trap: policy easing intended to stimulate growth instead reduces banks’ capacity to generate capital internally.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Empirical research on historical Chinese lending patterns shows end-of-month quota-driven lending spikes were associated with higher eventual default probabilities, particularly among state-owned enterprises. This suggests that prior credit expansion prioritized activity targets over underwriting discipline. The cumulative effect is capital quality degradation that cannot be reversed through rate adjustments alone.

Phase Mapping Within Our Strategy Framework

Current Alignment: Phase Two Compression (Probability: approximately sixty percent through June 2026).

Credit growth is decelerating toward six percent year over year, down from double-digit levels two years prior. January, typically the strongest month for new lending, failed to reaccelerate materially. This supports an ongoing compression regime rather than reflation.

Next Phase Risk: Escalation Toward Phase Three Stress (Probability: approximately twenty five percent by December 2026).

Escalation would involve visible recapitalization, broader property sector write-downs, or sharper deceleration in credit flows accompanied by rising defaults.

Policy Collision or Formal Restructuring: Phase Four Risk (Probability: approximately fifteen percent by June 2027).

This scenario would require explicit bank recapitalization, asset carve-outs, or monetization measures large enough to materially shift balance sheet constraints.

What Changes and What Does Not

What Changes:

- Loan growth continues to slow despite lower policy facility rates.

- Regulatory oversight intensity is increasing.

- Provincial growth targets are being revised lower.

What Does Not Change:

- Official non-performing loan ratios remain stable in reported data.

- The structural concentration of assets within state-dominated banks.

- Policy preference for containment over abrupt recognition of losses.

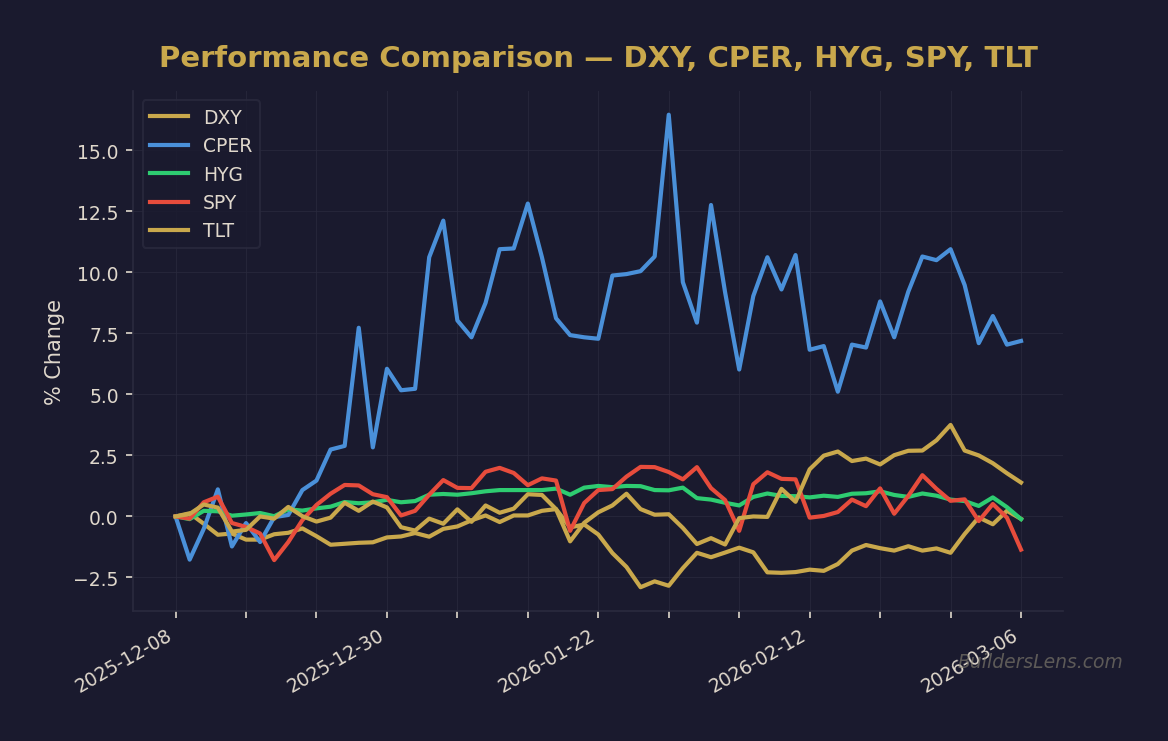

Multi-Asset Monitoring Implications

Rates: Persistent compression in China reduces global reflation probability and may support duration in deflationary risk scenarios.

Credit: Watch for spread widening or restructuring headlines in property-linked exposures.

Liquidity: Monitor changes in reserve management operations and implicit recapitalization tools.

Foreign Exchange: Renminbi stability versus dollar strength will indicate funding pressure transmission.

Market Internals: Copper, emerging market equities such as EEM, and global bank indices provide cross-confirmation signals.

Confirmation and Invalidation Conditions

Confirmation of Ongoing Constraint:

- Further deceleration in aggregate loan growth.

- Expansion of systemically important bank oversight.

- Formal reduction of national GDP targets.

Invalidation of Constraint Thesis:

- Transparent large-scale recapitalization.

- Broad-based private sector credit reacceleration without margin compression.

- Visible asset write-downs accompanied by renewed capital buffers.

Signal Confidence Tier

Signal confidence remains moderate to high in identifying a compression regime. Confidence decreases regarding timing of escalation, as policy containment mechanisms can extend duration. Our Strategy therefore emphasizes probability bands rather than deterministic outcomes.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze DXY (US Dollar Index)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.