Research · Credit & Liquidity

Commercial Real Estate Stress Is About Refinancing, Not Just Vacancy

Commercial Real Estate: Refinancing Arithmetic Meets Regulatory Sequencing

The current commercial real estate cycle is not defined solely by elevated vacancy rates.

The deeper mechanism is refinancing arithmetic intersecting with policy-driven capital

expenditure requirements. When debt reprices materially higher and operating margins

compress simultaneously, equity sensitivity increases nonlinearly.

Mechanism One: Debt Maturity and the Funding Cost Reset

A significant volume of commercial real estate debt is scheduled to mature into twenty

twenty seven. Properties financed in the low-rate environment of twenty twenty through

twenty twenty two must refinance at materially higher rates. The transmission channel is

straightforward: higher interest expense reduces distributable cash flow. If net operating

income does not grow proportionally, equity absorbs the adjustment.

This dynamic is most acute in office markets with structurally higher vacancy rates. Lower

occupancy reduces revenue resilience at the exact moment debt service increases.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Mechanism Two: Policy-Driven Conversion and Capital Mandates

Legislation streamlining office-to-residential conversion reduces zoning friction and

accelerates supply reallocation. Simultaneously, decarbonization and electrification

mandates introduce required capital expenditures over the next decade. For smaller,

leveraged operators, retrofit costs compound refinancing pressure.

The key variable is not political alignment but cost structure. Rising insurance, property

taxes, financing costs, and mandated upgrades converge into margin compression.

Phase Mapping Within Our Strategy Framework

-

Current regime: Phase Two multiple compression.

Elevated refinancing risk and softening rents in select markets, but no broad forced-liquidity

event yet. -

Probability through December twenty twenty six:

approximately sixty percent likelihood of continued contained compression. -

Next-phase risk Phase Three credit stress:

approximately thirty percent probability before June twenty twenty seven if credit spreads

widen and regional bank stress escalates. -

Low-probability tail Phase Four forced liquidity:

approximately ten percent over the same horizon, rising if labor deterioration coincides

with funding stress.

What Changes and What Does Not Change

What changes:

financing cost resets, capital expenditure requirements, and asset valuation sensitivity.

What does not change:

the primacy of credit spreads, funding conditions, and labor stability as systemic triggers.

Vacancy alone does not create systemic crisis; credit transmission does.

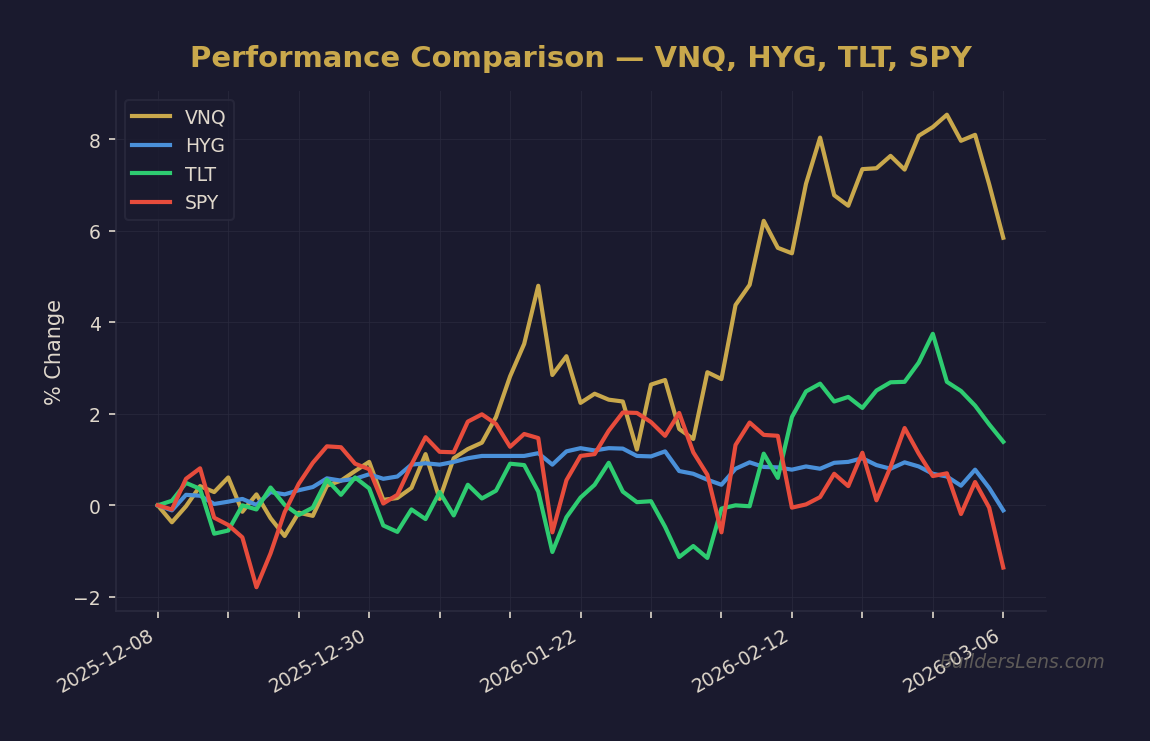

Multi-Asset Monitoring Framework

- High yield credit spreads, especially real-estate-exposed issuers

- Regional bank balance sheets and loan loss provisions

- Commercial mortgage-backed securities delinquency rates

- Long-duration Treasury yields as a refinancing-cost proxy

- Urban labor market deterioration indicators

Invalidation Conditions

- Sustained compression in credit spreads despite heavy debt maturities

- Stabilization or decline in long-term yields that reduces refinancing burden

- Office-to-residential absorption without triggering rent compression

Strategic Conclusion

The commercial real estate cycle currently reflects Phase Two compression rather than a

systemic collapse. The escalation pathway requires credit transmission into labor and

funding markets. Our Strategy prioritizes sequencing over prediction: we monitor refinancing

pressure, credit spreads, and policy-induced capital shifts to determine whether compression

remains contained or transitions into broader forced liquidity.

This analysis is educational and non-advisory, grounded in probability and signal-based

regime assessment.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.