Research · Market Internals

Defensive Rotation Is Rising Beneath the Surface

Defensive Rotation Beneath the Surface: Signal or Structural Shift?

The surface narrative says the index is stable. The internal structure says leadership is changing. Our Strategy prioritizes structure over headlines.

We are observing a meaningful rotation away from mega-cap technology and toward defensives, value, and hard-asset-linked sectors. This matters not because it predicts a crash, but because leadership deterioration often precedes regime transition.

Mechanism Over Narrative

When duration-sensitive growth stocks weaken while utilities, staples, energy, and materials strengthen, the market is reallocating toward cash flow durability and balance sheet resilience.

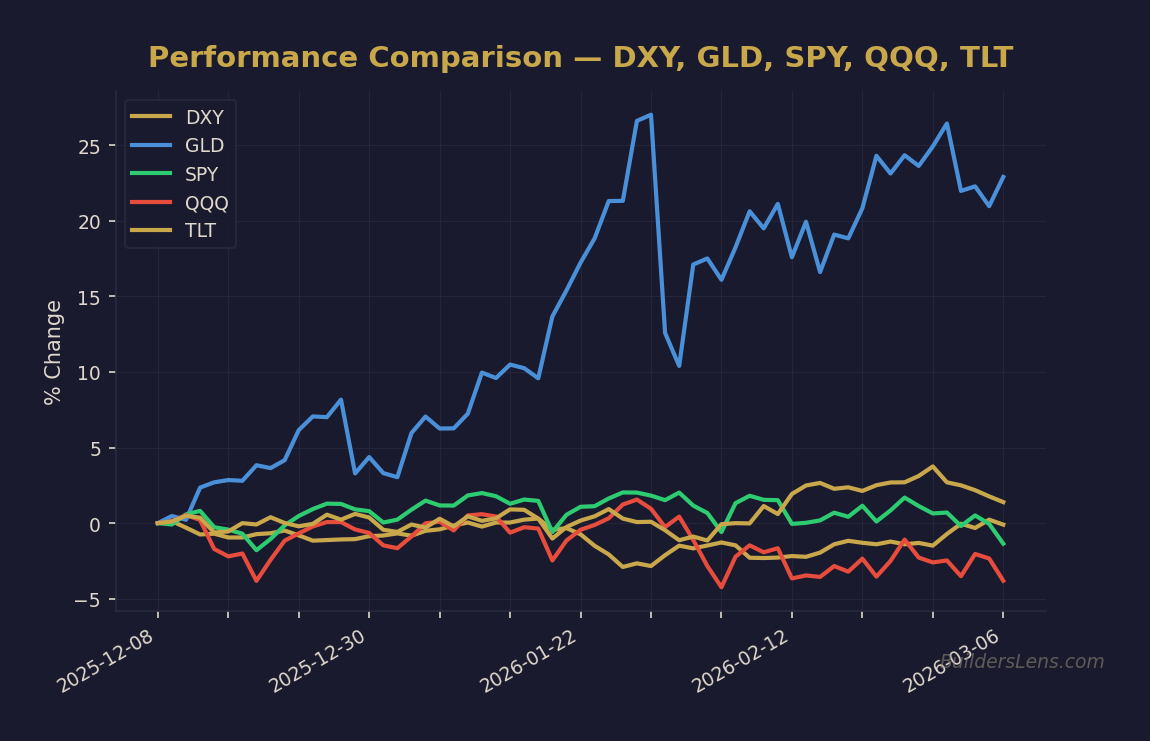

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

This is not inherently bearish. It can represent healthy broadening. However, it can also represent late-cycle multiple compression. The distinction depends on credit transmission and financial conditions.

Rates Are the Hinge Variable

Yields are trending lower. Lower yields can signal one of two things:

- Benign Disinflation: Growth moderates, inflation cools, policy expectations adjust, and credit remains stable.

- Emerging Stress: Growth deteriorates faster than expected, refinancing pressure rises, and spreads widen.

Falling yields alone are not confirmation of stress. Credit spreads, financial sector stability, and refinancing conditions determine escalation.

Market Internals: Dispersion Is Rising

We are seeing a “two-track” market. The percentage of stocks at new highs and new lows rising simultaneously indicates increasing dispersion.

Dispersion increases volatility risk because leadership becomes less cohesive. Cohesive leadership sustains trends. Fragmented leadership creates reversals.

This is characteristic of late Phase One transitioning toward Phase Two.

AI Capex and the Illusion of Strength

Growth data remains firm, but capital expenditure is heavily concentrated in AI-related spending. That concentration introduces fragility.

If AI investment maintains productivity gains, rotation remains orderly. If capital intensity fails to generate expected returns, earnings compression follows.

Concentration risk is not visible in headline GDP. It is visible in sector leadership divergence.

Dollar and Hard Asset Signaling

Gold strength and defensive outperformance reflect rising demand for real asset exposure. Meanwhile, the dollar remains range-bound but structurally sensitive.

A sustained dollar rally would tighten global liquidity. A structural dollar breakdown would reinforce hard asset leadership. For now, the dollar is a confirming variable, not a leading one.

Phase Mapping: Where We Stand

Current Phase: Late Phase One

Equities remain above major structural support. Credit is stable. Breadth has improved relative to narrow mega-cap dominance.

However, leadership deterioration and defensive rotation indicate rising pressure.

Next Phase Probability: Phase Two (Multiple Compression)

If mega-cap technology fails to regain leadership and yields continue declining, the probability of broader multiple compression increases.

Escalation Phase: Phase Three (Credit Transmission)

This requires widening spreads, financial breakdown, and refinancing stress. We are not there. But it remains a conditional tail risk.

Date-Anchored Probability Timeline

Through June 2026: Approximately 60 percent probability of continued rotation and range behavior with elevated volatility.

Through December 2026: Approximately 30 percent probability of sustained multiple compression if leadership does not reassert.

Into Mid-2027: Roughly 20 percent probability of deeper credit transmission, conditional on spread expansion and labor deterioration.

These probabilities update with confirmation or invalidation signals.

Confirmation Checklist

- Consumer discretionary underperforms staples persistently.

- Financials lose structural support.

- Investment-grade and high-yield spreads widen meaningfully.

- Dollar strength coincides with equity weakness.

- Mega-cap technology fails at prior resistance zones.

Invalidation Signals

- Semiconductors and mega-cap technology regain leadership.

- Credit spreads remain orderly despite yield declines.

- Financials stabilize and re-accelerate.

- Breadth expands without defensive dominance.

What Changes vs What Does Not

What Changes

- Leadership is no longer concentrated.

- Defensive sectors are outperforming.

- Rate expectations are being repriced.

What Does Not Change

- Credit remains stable.

- Equities are above major long-term support.

- No confirmed systemic liquidity event.

Strategic Posture: Optionality Over Conviction

Our Strategy does not predict. We sequence.

Rotation without credit stress argues for patience and flexibility. Escalation requires confirmation. Until then, we treat this as rising Phase Two pressure within a still-functioning system.

Volatility increases in transitional regimes. Optionality becomes more valuable than directional certainty.

Educational Note

This analysis is for informational and educational purposes only. It does not constitute investment advice. We frame probabilities, structural transitions, and macro mechanisms — not personal financial decisions.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)