Research · Macro Regime

Globalization Has Failed. What Replaces It?

Globalization Has Failed. What Replaces It?

When a superpower publicly declares that globalization has failed, that is not rhetoric. It signals structural transition. We are not observing isolated geopolitical events. We are observing the reinvention of the global operating system in real time.

From Liberal Order to Defensive Mercantilism

The prior system relied on persistent trade imbalances, free capital mobility, and financial asset inflation as stabilizers. Large US deficits were mirrored by large surplus nations recycling capital into US assets. That structure supported liquidity expansion, suppressed volatility, and masked domestic imbalances.

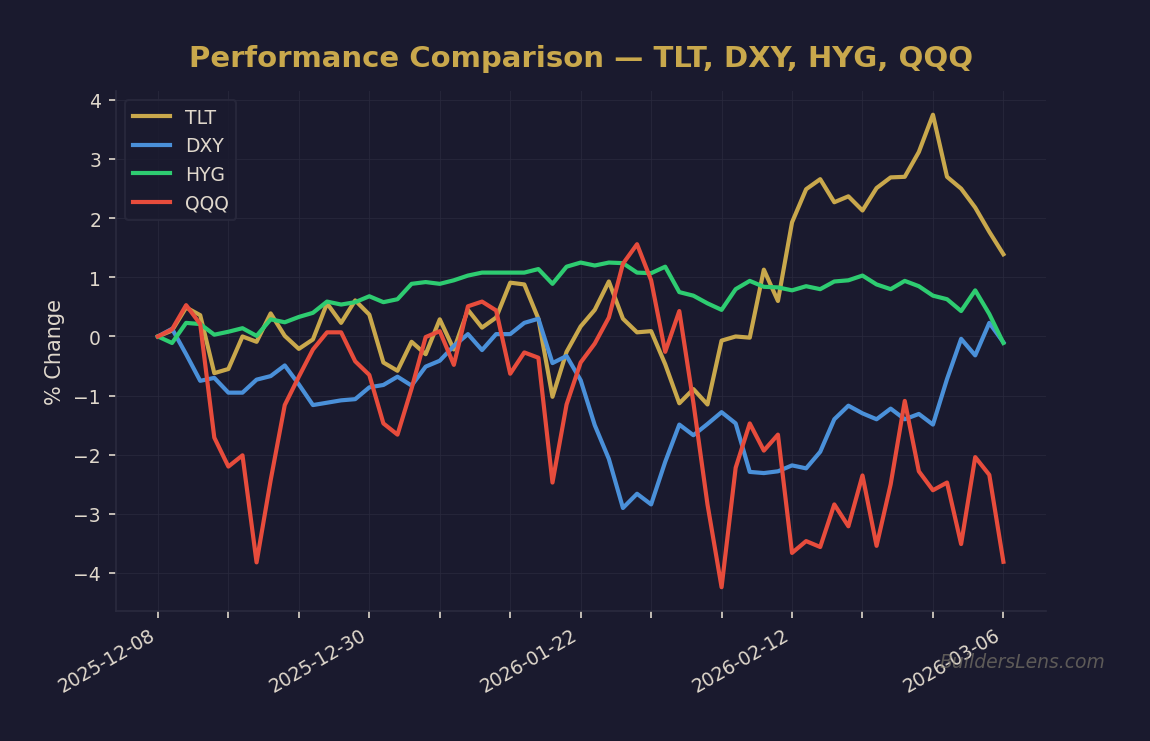

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

What is emerging now is not classical imperial mercantilism. It is defensive mercantilism. It centers on reindustrialization, capital redirection, supply chain security, and geopolitical alignment.

The mechanism matters more than the narrative. When trade deficits compress, capital flows change. When capital flows change, asset pricing adjusts. When asset pricing adjusts, volatility increases. Policy then becomes more active, not less.

Japan, Yields, and Transmission Risk

Japan’s rising government bond yields are not a local anomaly. They pressure global rate structures, influence currency volatility, and challenge the carry trade that has underpinned liquidity for decades.

If Japanese yields rise structurally, the transmission into US Treasuries alters global liquidity conditions. That shift feeds directly into credit spreads, equity multiples, and capital allocation decisions.

Taiwan, Geometry, and Strategic Alignment

Taiwan is not solely a semiconductor story. It is naval geometry, alliance architecture, and first island chain containment. The strategic value extends beyond technology into power projection and deterrence positioning.

The structural shift therefore ties industrial policy directly to military alignment.

Latin America and Regional Integration

Resource security is foundational to reindustrialization. Regional integration across the Americas reduces dependency risk and strengthens supply chain cohesion. That is not symbolic diplomacy. It is industrial input management.

Europe: Alignment or Fragmentation

Europe faces a structural choice. Align more deeply within a US-led industrial bloc, or pursue strategic autonomy without full fiscal and political integration.

We assign approximately 60 percent probability that Europe ultimately aligns rather than fractures. However, that path likely includes internal political turbulence extending into 2027.

Phase Probabilities and Timeline Anchors

As of February 2026, we assess:

- 55 percent probability of continued transition phase through June 2026, marked by volatility but no systemic fracture.

- 30 percent probability of accelerated bloc consolidation by December 2026.

- 15 percent probability of policy miscalculation triggering financial stress requiring coordination by June 2027.

These probabilities will adjust as confirmation signals evolve.

What We Are Monitoring

- Capital redirection from surplus nations into productive US investment rather than Treasury recycling.

- Acceleration in defense spending across Japan and Europe.

- Compression of US trade deficits.

- Sustained upward pressure in long-duration yields without systemic stress intervention.

Confirmations across these signals reinforce structural transition. Failure to confirm would suggest policy stall or reversion pressure.

The Dollar and Monetary Structure

A successfully implemented defensive mercantilist transition does not require a dollar collapse. It requires a managed range that supports reindustrialization without destabilizing capital markets.

Structurally, this implies more active capital management and potentially new monetary instruments reshaping cross-border liquidity geometry.

Commodities and Industrial Inputs

Reindustrialization increases strategic demand for commodities. However, because these inputs are systemically important, pricing will face intervention ceilings. Volatility is likely. Structural support does not imply unchecked upside.

Conclusion: Mechanism Over Narrative

The next decade will not resemble the last. Asset pricing will be driven less by passive liquidity expansion and more by capital allocation, industrial policy, and geopolitical alignment.

Our Strategy remains probability-based and confirmation-driven. We do not predict endpoints. We track structural phase pressure, monitor signal clusters, and recalibrate as evidence evolves.

Globalization may be fading. Systems do not disappear. They evolve. The transition phase is where volatility increases, but so does structural clarity for those observing the right signals.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze TLT (Long-Term Treasuries)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.