Research · Macro Regime

Growth Strong, Markets Fragile? The Late-Cycle Tension

Growth Is Holding. Fragility Is Rising.

Growth remains resilient. Inflation is drifting lower. Productivity gains are beginning to show up in the data.

On the surface, this resembles a constructive macro environment.

But markets are not reacting to the surface. They are reacting to internal pressure.

And beneath stable headline growth, fragility is beginning to build.

In Our Strategy, we focus on sequencing rather than timing, mechanisms rather than narratives,

and probabilities rather than predictions. The key question is not whether growth can persist temporarily —

it is whether the internal structure supporting that growth is strengthening or weakening.

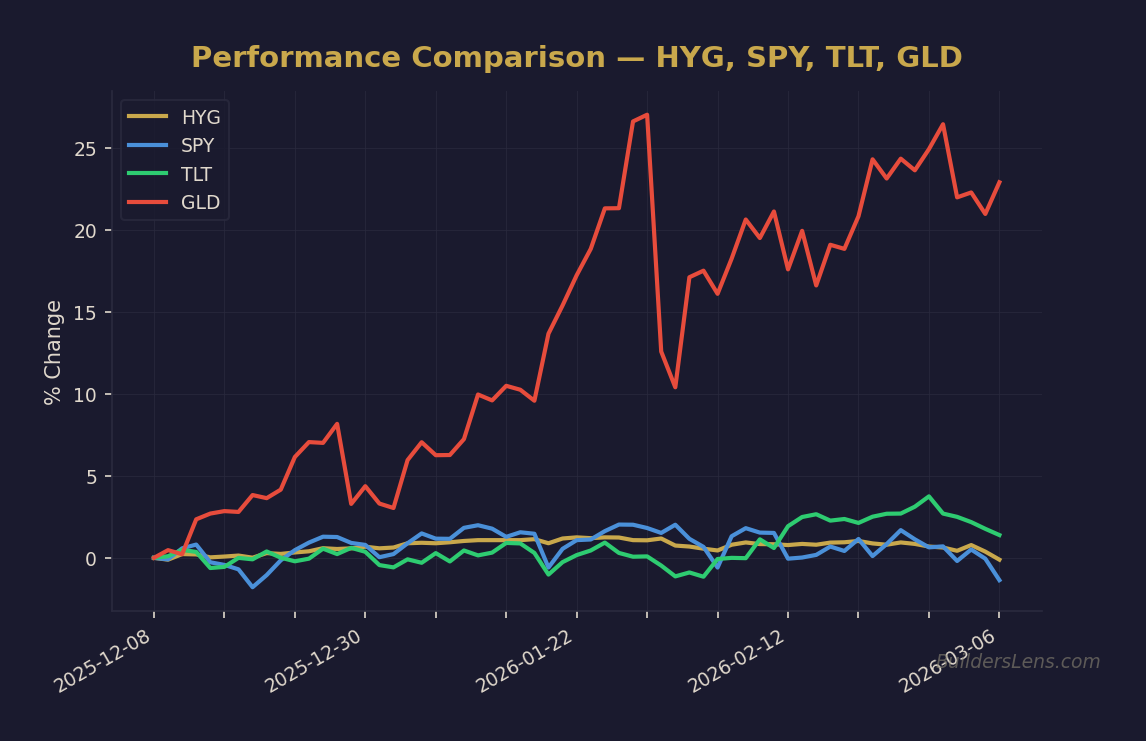

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

What Has Changed — And What Has Not

What has changed is not GDP strength. What has changed is concentration risk,

margin compression dynamics in AI-linked equities, and sensitivity to credit spreads.

What has not changed is that policy remains in delay mode. Liquidity has not collapsed.

Labor has not broken decisively. Credit stress has not yet accelerated.

That places us in late Phase Two of the operational framework —

a policy-delay regime where growth persists while internal volatility increases.

The Mechanism Beneath the Surface

AI Productivity vs Margin Compression

Productivity gains reduce unit labor costs. Lower unit labor costs can support disinflation.

That is constructive for the inflation narrative.

However, as AI adoption broadens, competitive pressure compresses margins.

When the most concentrated companies experience margin pressure, valuation sensitivity rises.

This is especially relevant when a small group of firms drive index performance.

Concentration is stability — until it becomes fragility.

Wealth Effect Transmission

If concentrated leadership corrects meaningfully, wealth effects transmit into services spending.

Higher-income cohorts drive discretionary demand: travel, leisure, recreation.

A 15 to 20 percent equity correction does not guarantee recession.

But it can reduce discretionary spending enough to slow services inflation and compress growth momentum.

Credit Is the Real Transmission Channel

Equity weakness alone is volatility. Equity weakness combined with widening credit spreads

becomes economic tightening.

Credit spreads are the mechanism that converts market stress into funding stress.

Funding stress affects hiring. Hiring affects income. Income affects consumption.

That is the sequence.

Phase Mapping: Where We Sit Now

Our Strategy’s five-phase model currently indicates elevated Phase Two pressure.

- Liquidity momentum: flat to modestly supportive

- Risk appetite: narrowing beneath index strength

- China divergence: marginal, not dominant

- Debt constraint pressure: gradually rising

We are not in confirmed Phase Three credit stress.

But the internal signals that precede Phase Three are becoming more frequent.

Probability Calibration

Next Three Months (Through June 2026)

- Phase Two continuation: 40 to 50 percent

- Controlled correction: 35 to 45 percent

- Disorderly credit transition: 10 to 15 percent

Next Six Months (Through December 2026)

- Late-cycle drift without crisis: 35 to 45 percent

- Phase Two to Phase Three transition: 40 to 50 percent

- Renewed reflation acceleration: 10 to 15 percent

Next Twelve Months (Through June 2027)

- Mild slowdown without systemic stress: 30 to 40 percent

- Credit-led reset sequence: 40 to 50 percent

- Sustained productivity-driven expansion: 15 to 20 percent

These are not forecasts. They are regime probabilities based on signal alignment.

Signals We Are Monitoring

Rates

- Ten-year yield direction and term premium behavior

- Auction demand quality

Credit

- High yield spreads

- Bank lending standards

Liquidity

- Balance sheet communication

- Funding market stability

Labor

- Hiring relative to break-even replacement levels

- Continuing claims trend

Market Internals

- Equal-weight versus cap-weight divergence

- Breadth deterioration

What Would Raise Phase Three Probability

- Sustained credit spread widening

- Hiring falling below replacement levels

- Liquidity tightening without coordination

- Equity correction spilling into funding markets

What Would Invalidate Fragility Concerns

- Broadening equity leadership

- Margin stability despite productivity expansion

- Credit spreads remaining historically contained

- Labor participation rising without unemployment acceleration

What Changes — And What Does Not

What Changes

- Tighter monitoring of concentration exposure

- Increased weight on credit spreads over index levels

- Shorter leash on late-cycle risk extensions

What Does Not Change

- No pre-positioning for recession without confirmation

- No narrative-driven exits

- No abandonment of optionality

- No all-in directional positioning

Delay Is Not Resolution

Policy delay can extend expansion. It can smooth volatility.

It can even produce late-cycle rallies.

But delay does not eliminate structural pressure.

The current regime is defined by coexistence: strong headline growth alongside rising internal fragility.

Our task is not to predict the break.

It is to monitor the sequence.

We do not need to be early.

We just cannot afford to be late.

For ongoing macro regime research, visit

builderslens.com.

Research support provided by

v6d.com.

This material is educational and not investment advice.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.