Research · Macro Regime

Housing Weakness Reveals the Labor Market Shift

Housing Weakness, Payroll Revisions, and Phase Pressure

January existing home sales declined sharply despite lower mortgage rates, and prior month data was revised lower. Seasonal explanations were offered. Mechanically, however, the transmission channel appears more structural. Housing demand depends less on marginal rate movements and more on perceived income stability.

When transaction volume contracts while borrowing costs fall, affordability is not the binding constraint. Stability is. That distinction matters for how markets sequence risk.

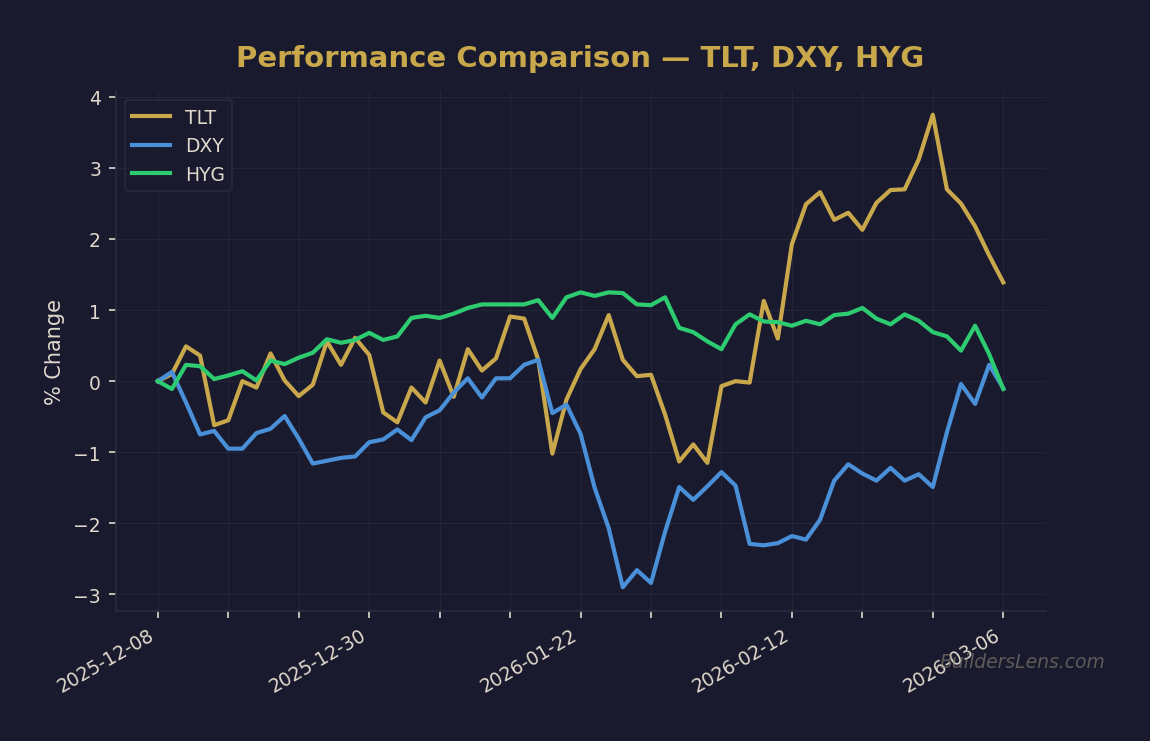

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

The Mechanism: Income Stability Over Rate Sensitivity

Housing transactions require long-duration financial commitments. Buyers commit to obligations that extend decades. Those commitments depend primarily on confidence in sustained income rather than short-term interest rate changes.

Recent payroll benchmark revisions suggest employment growth was materially weaker than initially reported. When adjusted for population growth and long-run labor force requirements, the employment gap appears to have widened over the past two years.

This does not imply mass layoffs. It implies persistent underperformance relative to trend. That underperformance behaves like a slow tightening in household confidence and purchasing capacity.

Transmission Pathways Across Asset Classes

- Treasuries: Lower yields reflect expectations of slower growth and labor softness beneath headline strength.

- Equities: Risk assets become vulnerable to multiple compression when employment momentum fades.

- Housing: Volume declines precede price adjustments and signal confidence deterioration.

- Credit: Early-stage delinquency increases in lower-income regions indicate localized strain rather than systemic crisis.

Framework Mapping: Our Strategy Phase Alignment

Current conditions align most closely with late Phase One (Melt-Up with Cracks) transitioning toward Phase Two (Multiple Compression and Rotation).

Phase Probabilities and Timeline Bands

- Phase One continuation through June 2026: Approximately 65 percent probability

- Phase Two dominant by December 2026: Approximately 25 percent probability

- Re-acceleration scenario through mid 2026: Approximately 10 percent probability if hiring stabilizes

- Phase Three credit stress risk by June 2027: Low but rising conditional probability if spreads widen materially

What Changes vs. What Does Not

What changes:

- Housing volume weakness now confirms sensitivity to labor stability.

- Bond markets appear to price slower growth more consistently.

- Regional delinquency concentration links housing stress to income distribution.

What does not change:

- No evidence of systemic mortgage crisis comparable to 2008.

- Credit markets remain functional; spreads are not disorderly.

- Broad employment collapse has not yet materialized.

Multi-Asset Monitoring Dashboard

- Rates: Ten-year yield trend and persistence of bull steepening

- Credit: High-yield spreads and private credit stress proxies

- Liquidity: Treasury auction strength and repo stability

- Foreign Exchange: Dollar strength as a global tightening signal

- Market Internals: Breadth deterioration versus narrow leadership

- Housing: Existing sales volume, builder sentiment, and regional delinquencies

Invalidation Conditions

- Sustained improvement in hiring rates and upward payroll revisions

- Rebound in housing transaction volume alongside stable credit spreads

- Re-acceleration in income growth without corresponding credit deterioration

Conclusion: Strain vs. Crisis

Current housing weakness reflects labor underperformance rather than rate constraint alone. The absence of mass layoffs does not eliminate contraction risk. Slow, cumulative employment gaps can generate persistent demand suppression.

Our Strategy remains sequencing-focused. If labor stabilizes, housing volume may recover gradually. If employment gaps widen further, Phase Two pressure increases and credit transmission becomes the next variable to monitor.

The distinction between strain and crisis will depend on the labor-to-credit feedback loop over the next twelve to eighteen months.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze TLT (Long-Term Treasuries)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.