Research · Credit & Liquidity

If Top Earners Pull Back, The Economy Reprices

If Top Earners Pull Back, The Economy Reprices

In Our Strategy, we operate with a five-phase macro framework and a simple discipline:

probabilities over predictions, sequencing over timing. Late in cycles,

headline strength can persist even as the underlying system weakens.

This analysis focuses on a specific late-cycle vulnerability: when spending power and

confidence among top earners begin to soften, aggregate demand can reprice faster than

headline data suggests.

What the Source Video Is Actually Claiming

The original discussion argues that surface-level resilience can mask deterioration

beneath the economy. Several themes stand out:

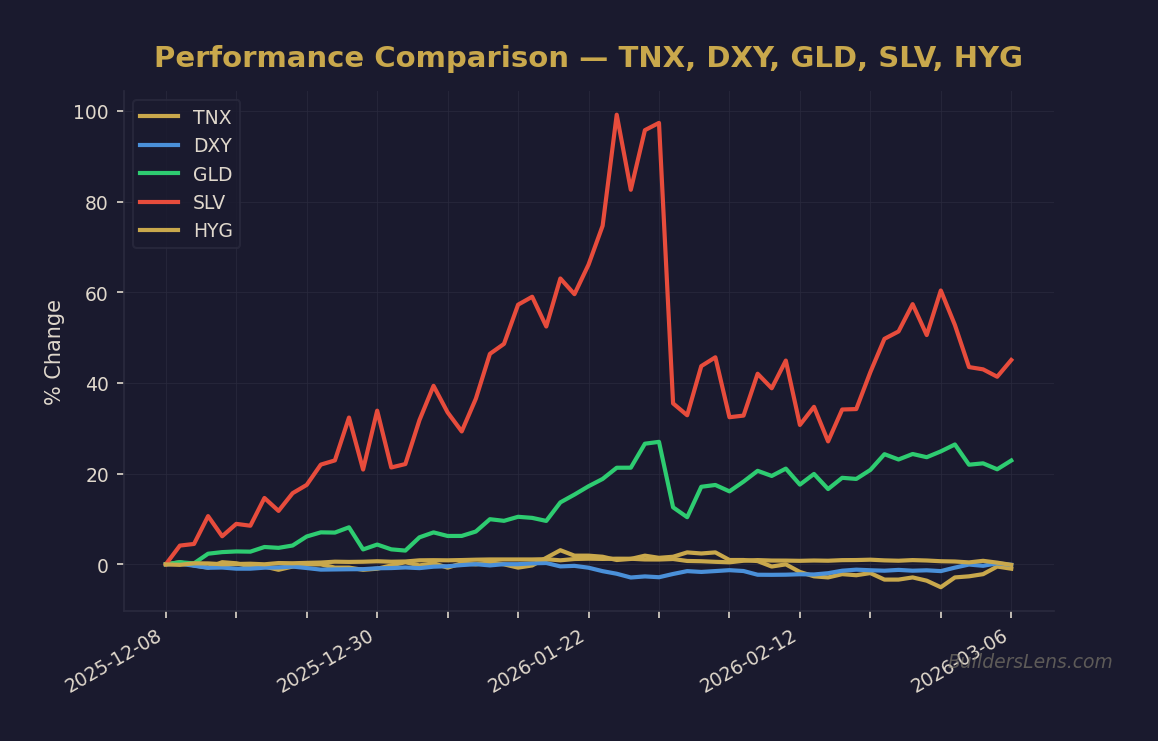

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

- Labor market quality is weakening even if headline unemployment remains stable

- Credit stress is rising through bankruptcies, distressed exchanges, and refinancing pressure

- A K-shaped economy matters because top earners drive a disproportionate share of spending

- Housing and shelter inflation may cool through rent normalization and price discovery

- Precious metals volatility reflects positioning and structure, not a straight-line hedge

The core claim is not imminent recession. It is that demand can reprice quickly if

high-income confidence and liquidity conditions shift.

Signal Classification Within Our Strategy

- Labor: Hiring quality, underemployment, and income concentration

- Credit: Refinancing stress, defaults, and oxygen constraints

- Yield direction: Policy expectations versus term premium pressure

- Liquidity plumbing: Volatility regime shifts and funding sensitivity

- Breadth & rotation: Defensive leadership as a late-cycle tell

- Real assets: Metals behavior as positioning and policy-risk signals

This is a Phase 1 signal with rising Phase 2 pressure, not a forced-liquidity trigger.

The Mechanism: Why Top Earners Matter Late Cycle

In a K-shaped economy, aggregate demand is increasingly driven by higher-income households.

When those households remain confident, spending can stay resilient even as lower-income

segments weaken.

The transmission risk emerges when:

- High-income job security or compensation growth slows

- Asset prices or liquidity conditions become less supportive

- Credit availability tightens at the margin

At that point, spending can retrench quickly. Labor data often confirms late, while credit

and funding conditions determine speed.

Phase Mapping: Where This Fits in the Cycle

Within Our Strategy framework, this discussion aligns with

late Phase 1: Melt-Up With Rising Fragility.

Index levels can remain elevated while labor quality and credit conditions deteriorate

underneath. A Phase 2 transition requires confirmation through credit, funding, or

earnings transmission.

Probability & Timeline Assessment (Non-Predictive)

-

Phase 1 continuation:

~55–65% probability through mid-2026 if liquidity and asset support persist. -

Transition toward Phase 2 conditions:

~25–35% probability by December 2026 if labor quality deterioration feeds into

credit stress. -

Phase 3 policy-dominant regime:

~15–25% probability by June 2027, conditional on tightening financial conditions

and funding pressure.

The key variable is not labor headlines, but whether labor weakness transmits into

defaults, earnings pressure, or funding stress.

What Changes in Our Strategy

- Greater weight placed on labor quality, not just unemployment rates

- Higher sensitivity to credit transmission as the accelerator mechanism

- Explicit monitoring of top-earner confidence as a demand driver

What Does Not Change

- No binary forecasts or all-in positioning

- No Phase 2 assumption without confirmation

- No elevation of narratives above signals

- No abandonment of tranche-based discipline and optionality

Signals We Continue to Monitor

- Yield direction across the 2Y, 10Y, and 30Y

- High-yield and investment-grade credit spreads

- Volatility regime behavior and funding sensitivity

- Dollar direction as a global constraint

- Equity breadth and defensive rotation

- Gold and silver behavior as policy-risk and positioning signals

Invalidation Conditions

- Sustained improvement in labor quality without credit deterioration

- Broad credit stabilization alongside easing financial conditions

- Renewed expansion in risk appetite with widening participation

Source

This article is for educational and informational purposes only. It reflects a

probability-based analytical framework and does not constitute investment advice

or recommendations.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning: