Research · Credit & Liquidity

Japan’s February 8 Decision: A Global Funding Signal, Not a Headline

Japan’s February 8 Decision: A Global Funding Signal, Not a Headline

In Our Strategy, we do not forecast outcomes. We translate macro developments into a probability-weighted,

phase-sequenced framework that prioritizes mechanisms over narratives.

The core question is not “Will Japan do something?” The core question is:

How does Japan’s funding regime transmit into global liquidity,

global term premium, and cross-asset risk appetite?

Strategy Anchor: How Our Strategy Thinks About This

Our Strategy is sequencing-first. Large market moves are usually driven by

liquidity and funding mechanics, then amplified through

credit reflexivity, and only later explained by narratives.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Japan matters because it has functioned as both a persistent source of cheap funding

and a major holder of U.S. Treasury assets.

This is not a Japan prediction. It is a signal translation:

when a global funding source reprices, it can tighten conditions elsewhere,

even if domestic data still looks stable.

What the Video Is Actually Claiming

The video argues that Japan’s February decision could affect U.S. markets through

several interconnected pathways.

- Japanese policy decisions influence domestic yields and financial stress.

- Yen-funded carry trades become less attractive if borrowing costs rise.

- Foreign demand for U.S. Treasuries may weaken, pushing yields higher.

Our task is to map those claims into signal buckets, mechanisms, and phase pressure

without turning them into predictions.

Signal Classification: Where This Fits in Our Signal Stack

Rates and Term Premium

Japan’s yield regime affects relative asset attractiveness and global portfolio rebalancing.

Rising Japanese yields can place upward pressure on global long-term rates.

Dollar and Global Funding Stress

The yen has served as a low-cost funding currency.

When funding currencies reprice, unwinds are often nonlinear.

Liquidity Plumbing

This is not abstract liquidity. It is about balance sheets, auction clearing,

and marginal buyers of sovereign debt.

If foreign demand weakens, yields must adjust.

Credit and Housing (Second Order)

Japan’s variable-rate mortgage structure matters domestically.

We treat it as an amplifier rather than the primary global transmission channel.

Mechanism: The Transmission Path That Matters

Japan as a Global Funding Source

Ultra-low Japanese rates created incentives to borrow cheaply and deploy capital elsewhere.

This subsidized global risk-taking for years.

When Rates Rise, Incentives Shift

Higher Japanese rates reduce carry profitability.

Positions tend to persist until thresholds are crossed.

Unwinds Occur During Volatility

Markets often remain calm while incentives deteriorate.

When volatility rises, positions unwind quickly.

Treasury Demand as a Clearing Variable

If Japanese investors reallocate domestically,

U.S. yields may rise to clear heavy issuance.

Why Markets Misread This

The headline decision is an event.

The yield and funding response is a process.

Phase Mapping Within Our Five-Phase Framework

- Phase 1: Melt-up with growing fragility

- Phase 2: Multiple compression and rotation

- Phase 3: Breakdown and credit stress

- Phase 4: Forced liquidity and policy collision

- Phase 5: Stabilization and accumulation

The Japan signal primarily raises Phase 1 and Phase 2 pressure.

It does not independently confirm Phase 3 or Phase 4.

Probability and Sequencing Windows

Current Probabilities

- Phase 1: 50–60%

- Phase 2: 25–35%

- Phase 3: 10–20%

- Phase 4 tail risk: 5–15%

June 2026

If yields rise and auctions weaken, Phase 2 probability increases.

December 2026

Persistent rate pressure raises Phase 3 risk.

June 2027

If stress resolves through policy and liquidity,

Phase 5 stabilization becomes plausible.

What Changes and What Does Not

What Changes

Japan becomes a higher-weight monitoring node for global rates and funding.

What Does Not Change

- No phase shifts on a single event

- No crash assumptions

- No abandonment of confirmation discipline

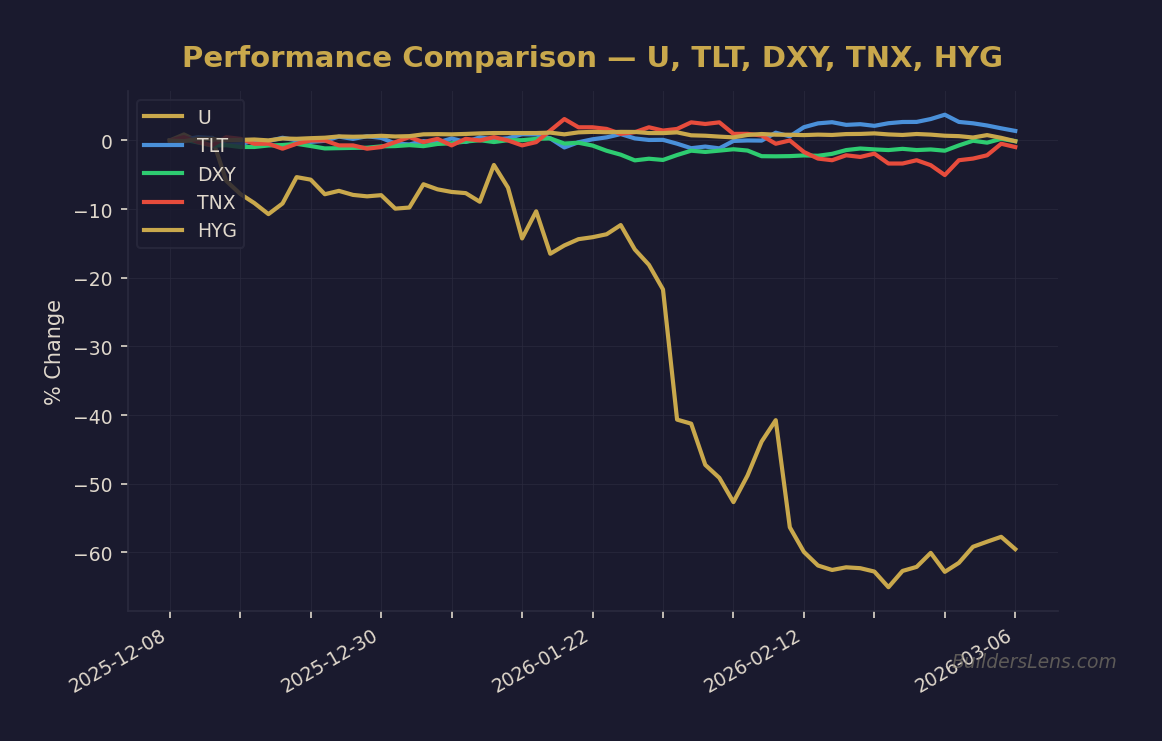

Monitoring Dashboard (Observation Only)

- USDJPY

- JGB 10-year yield

- TNX

- TLT

- HYG and JNK

- DXY

- VIX

Confirmations and Invalidations

Confirmations

- Persistently higher Japanese yields

- Weak U.S. Treasury auctions

- Rising U.S. long-term yields

- Credit spreads widening

Invalidations

- Japan resumes easing

- Yields fall sustainably

- Credit remains stable

Closing Discipline

Japan’s decision is not a prediction trigger.

It is a lens into global funding conditions.

We do not need to be early.

We just cannot afford to be late.

This content is for educational purposes only and does not constitute investment advice.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

The source video we are translating and pressure-testing is here:

Japan’s February 8 Decision Could Flip the U.S. Stock Market (Here’s Why)

.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)