Research · Cycle Sequencing & Phases

Labor Data Is Not Confirming a Rebound Narrative

As 2026 begins, a dominant narrative continues to circulate: the U.S. economy and labor market are stabilizing and poised for reacceleration. Our Strategy does not evaluate that claim through sentiment or forecasts. We evaluate it through signal alignment, transmission mechanisms, and phase pressure.

The latest labor data does not confirm a clean rebound. Instead, Challenger job cuts, revised ADP employment trends, and JOLTS labor turnover are converging in a way that raises late-cycle fragility rather than resolving it.

Why Labor Matters Late Cycle

Labor is rarely a leading signal early in the cycle. It becomes decisive late in the cycle when it begins to transmit through household income, spending behavior, and credit performance. That transmission, not the headline payroll number, is what Our Strategy monitors.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

When hiring slows, hours soften before layoffs accelerate. When hours decline, disposable income weakens even if employment levels appear stable. This is how labor stress begins to influence demand, margins, and eventually credit quality.

The Current Labor Signal Cluster

The current concern is not any single data series. It is the clustering of multiple labor indicators pointing in the same direction.

Challenger job cut announcements surged while hiring intentions collapsed. These announcements reflect forward-looking corporate behavior rather than backward-looking counts. Plans set at the end of 2025 imply employers are not positioning for expansion.

ADP benchmark revisions reframed the timeline of labor weakness. Job losses now appear to have begun much earlier than mainstream narratives acknowledged, aligning more closely with prior bond market behavior.

JOLTS data, while noisy, continues to show falling job openings and repeated episodes of negative net labor turnover. Hiring is failing to absorb quits and separations. That condition is inconsistent with a strengthening labor market.

Transmission Into Markets: Why Risk Reacts First

Markets do not wait for official recession labels. They respond to changes in optionality and liquidity sensitivity.

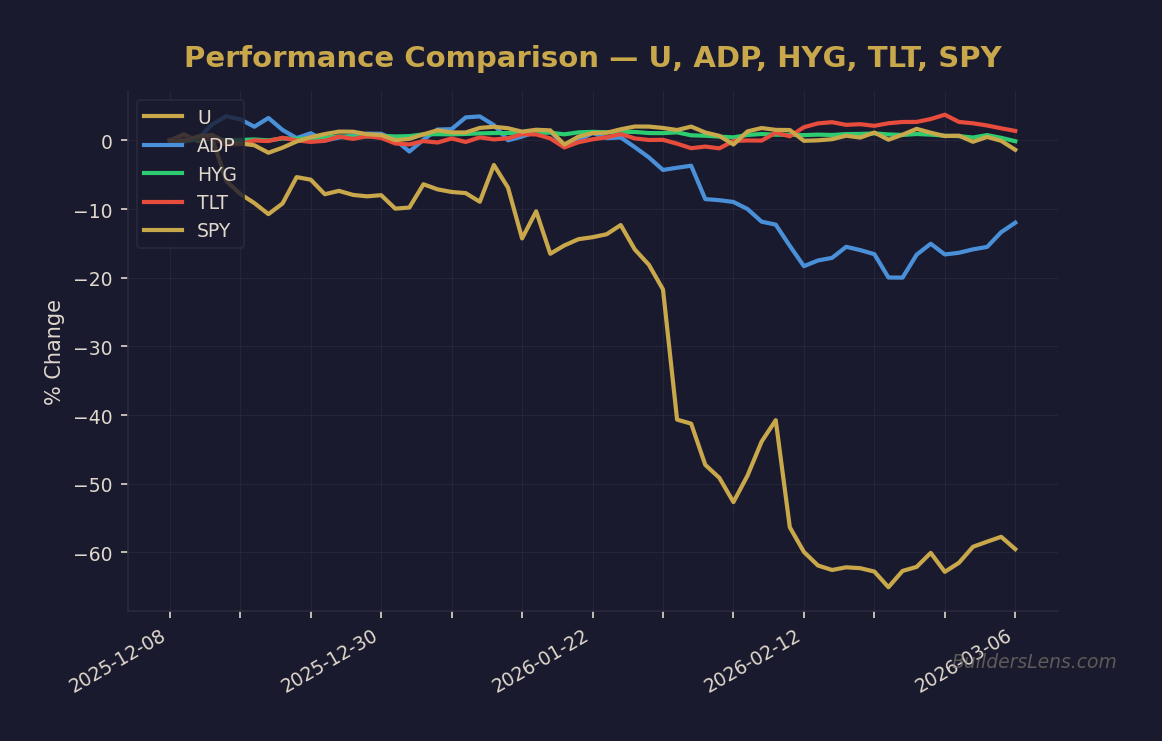

It is not coincidental that the sharpest reactions occurred in crypto, high-beta equities, and private credit proxies. These segments are most sensitive to funding conditions and refinancing assumptions. They price fragility before broader equity indexes adjust.

Our Strategy treats private credit as a transmission amplifier, not a causal origin. When labor softness weakens cash flow while lending standards tighten, credit stress can escalate quickly. That interaction matters far more than any single default statistic.

Phase Framework Placement

Within Our Strategy framework, the current configuration maps to late Phase 1 with rising Phase 2 pressure.

Phase 1 fragility allows markets to remain elevated even as internals deteriorate. Phase 2 emerges when valuation support weakens and risk appetite compresses, often without an immediate recession narrative.

Labor weakness alone does not trigger a phase transition. Labor weakness combined with tightening credit and deteriorating liquidity does.

Probability Pathways (Date-Anchored)

Our Strategy assigns probabilities to scenarios rather than forecasts outcomes. As of February 2026, we frame the next phases as follows:

- Phase 1 continuation with rising fragility through June 2026: approximately 45 to 60 percent

- Phase 2 multiple compression and rotation by December 2026: approximately 30 to 45 percent

- Phase 3 stress dominated by credit transmission by June 2027: approximately 15 to 30 percent

These probabilities will adjust as confirmation or invalidation emerges.

What Would Confirm Rising Phase Pressure

- Continued claims trending persistently higher

- Average weekly hours declining further

- Credit spreads widening and remaining wide

- Lending standards tightening alongside weaker loan demand

- Refinancing stress increasing in private credit and leveraged loans

What Would Invalidate This Setup

- Sustained reacceleration in hiring across sectors

- Stabilization or recovery in hours worked

- Credit remaining broadly available with compressing spreads

- Funding conditions improving without emergency intervention

What Changes and What Does Not

What changes in Our Strategy is discipline. As fragility rises, we raise confirmation thresholds, tighten risk tolerance in crowded exposures, and place greater weight on credit behavior.

What does not change is our refusal to convert tension into prediction. We do not make crash calls, and we do not chase narratives. We remain probability-driven, phase-aware, and optionality-focused.

Conclusion

The labor data is not delivering a resolution. It is delivering confirmation pressure. Markets can ignore that pressure for a time, especially when liquidity expectations dominate. But late in the cycle, the cost of misreading labor transmission increases.

Our Strategy does not require being early. It requires avoiding being late.

Educational disclaimer: This content is for informational and educational purposes only and does not constitute financial advice.

For ongoing macro strategy research, visit builderslens.com. This research is made possible by our sponsor v6d.com.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.