Research · Credit & Liquidity

Primary Dealers, Repo Stress, and the Quiet Rise in Phase Two Pressure

Recent developments across private credit and wholesale funding markets are not isolated events. They are mechanisms interacting. Our Strategy prioritizes plumbing over narrative, and the plumbing is sending signals.

Primary Dealer Treasury Accumulation: Defensive Collateral Positioning

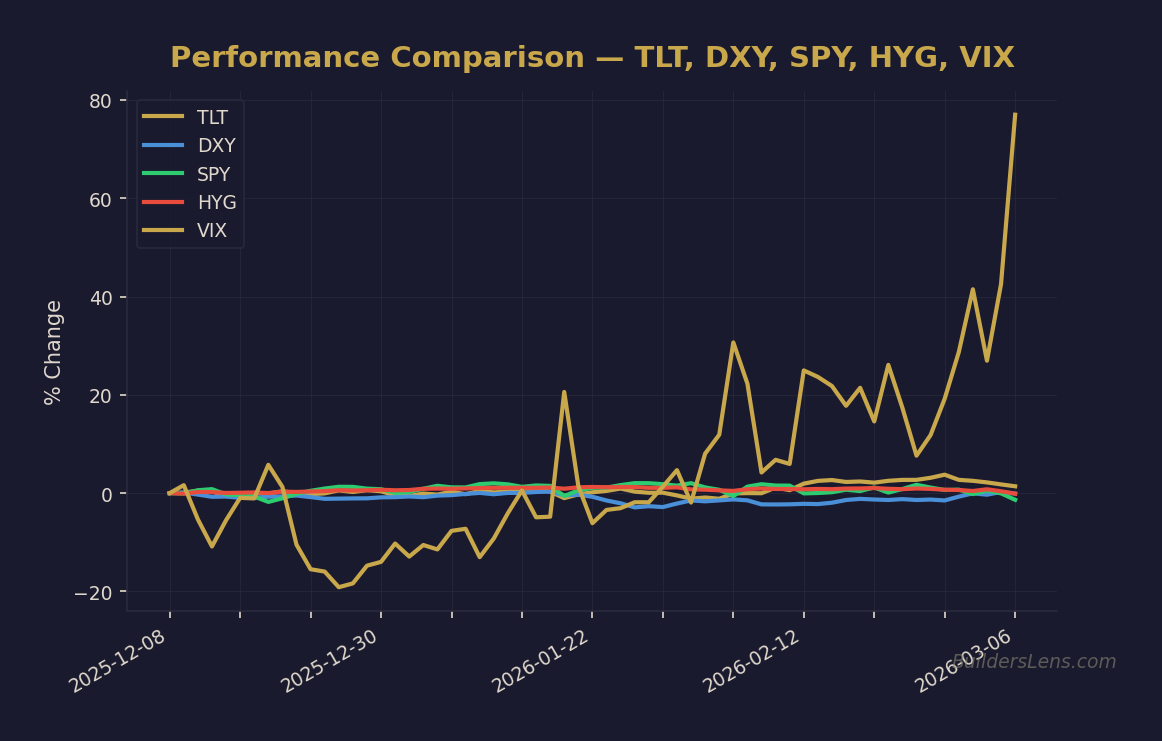

Primary dealer holdings of Treasury notes and bonds recently rose above four hundred billion dollars, marking a historic high. Dealers do not accumulate collateral in size without reason. This behavior typically reflects anticipation of tighter funding conditions, reduced collateral circulation, or expected stress in money markets.

Mainstream commentary often attributes rising dealer inventories to failed Treasury distribution. However, pricing behavior does not support forced absorption. Instead, the accumulation appears voluntary and defensive — a strategic positioning ahead of potential collateral scarcity.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Repo Facility Usage: A Quiet Circulation Constraint

After weeks of near-zero activity, borrowing at the Federal Reserve repo facility surged toward thirty billion dollars. Repo usage is a circulation signal. When private funding channels tighten, borrowers migrate to official backstops.

Cash and collateral are inseparable in wholesale markets. When collateral flow tightens, cash circulation follows. Rising dealer inventories combined with renewed repo borrowing increases the probability of systemic tightening rather than localized noise.

Private Credit Stage Two Behavior

The forced asset sales and gating actions observed within private credit are consistent with early stage two behavior in our framework. In stage one, outflows are offset by new investor capital or bank credit support. In stage two, those offsets weaken. Banks reduce incremental exposure. Liquidity buffers are drawn down. Asset sales become necessary.

The Federal Open Market Committee’s recent minutes referencing vulnerabilities in private credit further confirms that these risks are on institutional radar.

Phase Mapping Within Our Strategy Framework

Current Assessment — Late Phase One to Early Phase Two

We currently assign approximately sixty five percent probability that markets remain within late Phase One or early Phase Two conditions through June twenty twenty six. Liquidity has not fully broken, but pressure is building beneath surface calm.

Escalation Risk — Phase Three Funding Stress

We estimate roughly twenty five percent probability that Phase Three funding stress emerges before December twenty twenty six. This would require confirmation via sustained repo facility usage, widening credit spreads, continued dealer collateral accumulation, and labor market deterioration.

Forced Liquidity Window — Phase Four

Near-term probability of a full Phase Four forced-liquidity cascade remains approximately ten percent. However, this probability rises meaningfully if collateral hoarding persists while auction demand weakens and private credit stress spreads.

Phase Five Stabilization

A durable Phase Five stabilization window would likely require either coordinated policy intervention or observable normalization in credit spreads, dealer inventories, and repo usage metrics.

Multi-Asset Monitoring Dashboard

- Rates: Ten-year and thirty-year Treasury yield behavior; term premium trends.

- Credit: High-yield spreads; private credit fund flows; bank lending standards.

- Liquidity: Repo facility usage; dealer inventory trends; Treasury auction tails.

- Foreign Exchange: Dollar strength as global funding constraint.

- Market Internals: Breadth deterioration; volatility regime shifts.

What Changes vs. What Does Not

What changes: Funding stress probability has increased due to the convergence of dealer positioning, repo activity, and private credit asset sales.

What does not change: Our Strategy remains sequencing-first. We do not front-run Phase Four. We wait for confirmation of forced-liquidity mechanics before deploying aggressive capital.

Invalidation Conditions

- Repo facility usage returning to near-zero baseline for multiple consecutive weeks.

- Primary dealer Treasury inventories declining meaningfully.

- High-yield credit spreads compressing to prior tight ranges.

- Stable or improving Treasury auction demand metrics.

Signal Confidence Tier

This assessment reflects moderate confidence in rising Phase Two pressure, with low confidence in immediate Phase Four escalation. Mechanisms suggest tightening. Confirmation requires sustained follow-through in funding markets.

As always, our approach remains educational and non-advisory. We track signals, not stories.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.