Research · Credit & Liquidity

Private Credit Stress Is Rising — What It Signals in Our Five Phase Framework

Markets can look stable while the credit layer quietly gets more fragile. In this episode of Independent by Design — The Builders Lens, we translate a wave of “private credit is breaking” claims into mechanical signals inside Our Strategy’s five-phase framework — focusing on what would confirm stress, what would invalidate it, and which assets tend to feel it first.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Quick Disclaimer

This content is for educational and informational purposes only and reflects Our Strategy’s process — not financial advice. We use probabilities, sequencing, and confirmation — not predictions.

Source We Reviewed (Credit)

Our video on our channel (embedded above):

https://youtu.be/us5fskrnaFs

Original video referenced in our episode:

BlackRock’s Credit Collapse Forces MASS LAYOFFS | Crisis Just Began

Strategy Anchor: Why We Watch Credit Before Headlines

Our Strategy treats credit as a “transmission layer.” If private credit starts tightening, it often shows up in funding behavior, underwriting appetite, and spreads before equities admit anything is wrong.

Plain-English causality: This is happening because lenders get more protective when uncertainty rises, and when that happens it usually leads to fewer deals, tougher terms, and slower risk-taking across the system.

What the Video Is Really Saying (In One Line)

The claim isn’t “crash tomorrow.” The claim is: private credit is showing early-cycle stress behaviors (requests for cash back, tighter structures, and more caution), even while public markets can stay calm.

Key Takeaways We Extracted (Signal-First)

1) Private credit is a leading indicator — but it’s also opaque

Direction: Stress signals appear earlier than most people expect.

Magnitude: Often small at first — and then nonlinear if outflows and refinancing collide.

Relationship: Private credit can “look fine” until liquidity needs force selling or lenders pull terms.

Implication: We treat it as early warning, not as a timing tool.

Plain-English causality: This is happening because private loans don’t trade every second like stocks, and when that happens it usually leads to losses showing up late — after the behavior has already changed.

2) Mechanical indicators matter more than narrative

We’re less interested in single headlines (or one scandal story) and more interested in repeatable “plumbing” signs:

- Fee waivers and incentives to retain capital

- Covenant / coverage tests tightening

- Redemption pressure, gating language, or slower repayment cadence

- BDC performance vs. broader risk assets (as a public-market proxy)

- Credit spreads and refinancing terms (the public confirmation layer)

Plain-English causality: This is happening because managers try to stop money from leaving when confidence slips, and when that happens it usually leads to “soft restrictions” before “hard restrictions.”

3) Why credit can weaken before equities

Direction: Credit tightens at the margin first.

Magnitude: Early tightening can look trivial — until it hits refinancing windows.

Relationship: When marginal credit gets picky, growth and buybacks can slow later, which eventually pressures equity multiples.

Implication: Equity melt-ups can continue, but exits can get tighter and tail risk can rise.

Plain-English causality: This is happening because credit is the system’s oxygen, and when that happens it usually leads to fewer “second chances” for weaker borrowers.

Our Strategy Lens: Mapping This to the Five-Phase Framework

Based on the summary signals in the episode, we treat this as late Phase 1 behavior with a modest upward nudge to Phase 2 risk — conditional on confirmation.

What Changed

- Phase 2 pressure: up modestly if private-credit tightening persists and spills into public spreads.

- Signal stack priority: we move credit mechanics and funding conditions higher than “headline catalysts.”

- Process stance: tighten exit discipline and avoid assuming liquidity will always be available.

What Didn’t Change

- We do not treat this as a crash call.

- We do not time markets off a single story.

- We still require confirmation from spreads, funding, and labor before upgrading to “forced selling” conditions.

Transmission Path: How This Could Spread (If It Does)

- Private credit redemption pressure rises → managers get defensive.

- Deal terms tighten → weaker borrowers lose refinancing flexibility.

- BDC / high-yield signals wobble → public markets start pricing risk.

- Spreads widen + funding tightens → equities begin repricing (often abruptly).

Plain-English causality: This is happening because lenders protect their balance sheets when cash demand rises, and when that happens it usually leads to slower lending and higher borrowing costs across the economy.

Phase & Probability Update (Process View, Not Prediction)

Below is a template-style probability framing based on the signal described in the episode. This is not a forecast — it’s how we’d size the risk of regime change if confirmations arrive.

| Horizon | Phase 1 (Melt-up w/ cracks) | Phase 2 (Forced liquidity risk) | Phase 3 (Policy response / reset) | What Would Confirm Next |

|---|---|---|---|---|

| 3 months | Higher probability | Modestly higher | Low | BDC weakness, early spread widening, tighter underwriting |

| 6 months | Still plausible | Rising if credit confirms | Low-to-moderate | Spreads + funding stress + weaker labor |

| 9 months | Lower if spreads widen | Higher if refinancing bites | Moderate if stress compounds | Defaults rising, refinancing gaps, dealer/funding constraints |

| 12 months | Depends on liquidity | Meaningful risk if confirmed | Higher if policy forced | Policy shift, bailout talk, or clear recession confirmation |

Who This Hits First (If It Continues)

- Levered or refinancing-dependent borrowers (floating-rate exposure and weak coverage).

- Illiquid vehicles that promise liquidity mismatched to underlying loans.

- High-beta equities if spreads widen and correlations rise.

- Lower-quality credit (high yield, weaker BDCs) before broad index damage shows up.

Plain-English causality: This is happening because the weakest balance sheets feel tighter terms first, and when that happens it usually leads to stress spreading outward from the margins.

Viewer Playbook (Process Only — Not Advice)

- Separate narrative claims from confirmation signals (spreads, funding, underwriting).

- Track proxies: credit spreads, BDCs, and any visible deal/issuance hesitation.

- Expect nonlinear moves: “calm” can persist, then shift quickly if liquidity thins.

- Keep optionality high: avoid being forced into decisions by leverage or illiquidity.

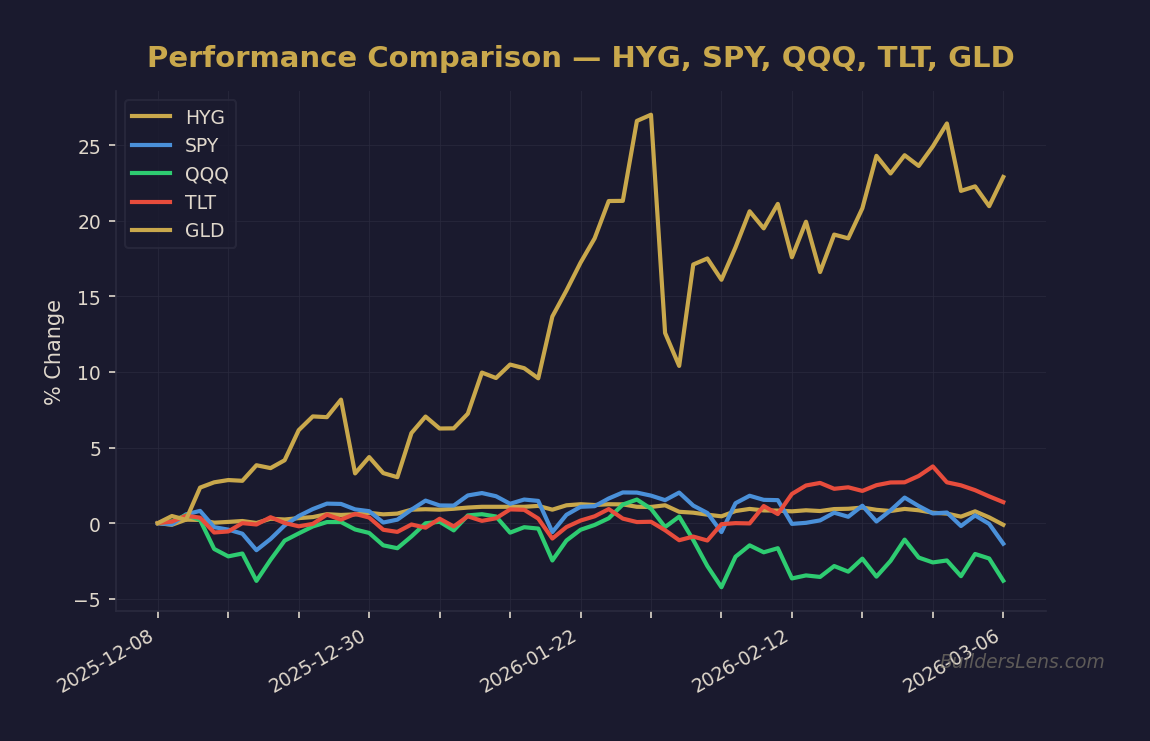

Ticker Sensitivity Watchlist (Monitoring, Not Recommendations)

If private credit stress spreads, these are often sensitive “dashboard” instruments:

- Credit / risk: BDCs (category), high-yield credit (category)

- Equity beta: SPY / QQQ (broad risk gauges)

- Rates response layer: TLT / ZROZ (duration sensitivity if growth breaks)

- Trust / hedge layer: Gold / Silver (if confidence and policy credibility deteriorate)

Close

Our bottom line: the signal is worth respecting, but the narrative is not the timing tool. We treat private credit as a leading “fragility” indicator — and we wait for confirmation in spreads, funding, and labor before declaring a phase shift.

If you want to watch the full episode, it’s embedded at the top. And if you want the source context, use the original link above and compare the claims to the confirmation checklist.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.