Research · Credit & Liquidity

Private Credit Stress Is Spreading Beyond “Cockroaches”

Private Credit Stress Is Spreading Beyond Early Weak Spots

In Our Strategy, we prioritize sequencing over prediction.

Credit cycles rarely fail all at once. They deteriorate unevenly, with stress

first appearing in weaker structures before testing the system more broadly.

The key question is not whether isolated problems exist. It is whether stress

is moving from valuation debate into liquidity necessity.

What the Source Video Is Actually Claiming

The source video argues that private credit stress is no longer confined to

isolated borrowers or niche structures. What began as early warning signs has

broadened across sectors and vehicles.

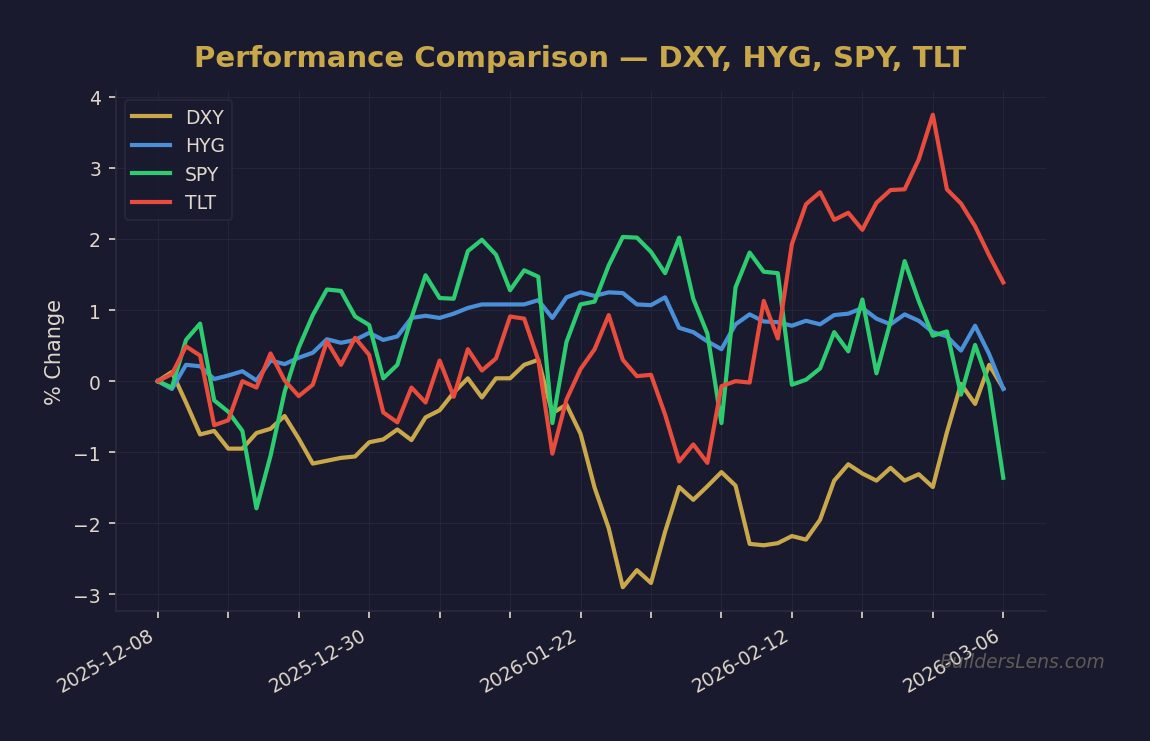

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

- Multiple private credit managers and BDCs repricing simultaneously

- Leveraged loan behavior deteriorating alongside private credit proxies

- Large capital expenditure funding needs acting as stress tests for credit availability

The claim is not that a collapse is underway, but that the margin for error in

private credit financing is narrowing.

Signal Classification Within Our Strategy

- Credit: Private credit marks, leveraged loan pricing, and recovery assumptions

- Liquidity: Redemption pressure, refinancing gaps, and funding access

- Rates & yields: Long-end behavior as a constraint on refinancing math

- Market structure: Public proxies as early sentiment and liquidity indicators

This is a Phase 1 credit deterioration signal with rising Phase 2 pressure,

not yet a forced-liquidity confirmation.

The Mechanism: How Credit Stress Becomes Systemic

Early in a credit downturn, stress shows up as mark-to-model debate.

Valuations can be defended as long as liquidity remains available.

The transition occurs when:

- Redemptions or funding needs force asset sales

- Refinancing becomes unavailable or prohibitively expensive

- Recovery assumptions are revised lower across portfolios

At that point, stress shifts from perception to mechanics. Liquidity, not

narrative, determines outcomes.

Phase Mapping: Where This Fits in the Cycle

Within Our Strategy framework, this signal set aligns with

late Phase 1: Fragility Beneath Stable Index Levels.

Phase 2 behavior requires visible forced-liquidity dynamics—redemptions,

emergency financing, or disorderly repricing—not just broader awareness

of risk.

Probability & Timeline Assessment (Non-Predictive)

-

Phase 1 continuation with elevated credit fragility:

~55–65% probability through mid-2026 if funding remains accessible. -

Transition toward Phase 2 conditions:

~25–35% probability by December 2026 if redemption pressure or refinancing

stress persists. -

Phase 3 policy-dominant regime:

~15–25% probability by June 2027, conditional on tightening financial

conditions and forced selling.

Credit stress raises risk density, but liquidity determines timing.

What Changes in Our Strategy

- Greater weight on credit-proxy confirmation across public and private markets

- Higher sensitivity to redemption pressure and emergency funding needs

- Increased emphasis on funding sources rather than borrower narratives

What Does Not Change

- No assumption of Phase 2 behavior without forced-liquidity evidence

- No extrapolation from single stocks or isolated headlines

- No abandonment of probability-based sequencing

- No erosion of optionality while liquidity remains available

Signals We Continue to Monitor

- High-yield and leveraged loan spread behavior

- BDC and private credit manager relative performance

- Redemption terms, emergency financing, and restructuring headlines

- Long-end yield behavior and refinancing math

- Dollar strength as a global liquidity constraint

Invalidation Conditions

- Stabilization in private credit marks alongside renewed issuance

- Compression in leveraged loan and high-yield spreads

- Broad improvement in funding conditions without policy distortion

Source

This article is for educational and informational purposes only. It reflects a

probability-based analytical framework and does not constitute investment advice

or recommendations.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze DXY (US Dollar Index)