Research · Market Internals

Silver’s Breakdown Was a Structure Signal, Not a Surprise

Silver’s Breakdown Was a Structure Signal, Not a Surprise

In Our Strategy, we treat sharp commodity moves as questions of mechanism first, not conviction. Silver’s recent reversal fits a familiar late-cycle pattern: supply-driven scarcity meets speculative momentum, then reverses as conditions normalize.

The Core Mechanism: Supply Squeezes Are Self-Resolving

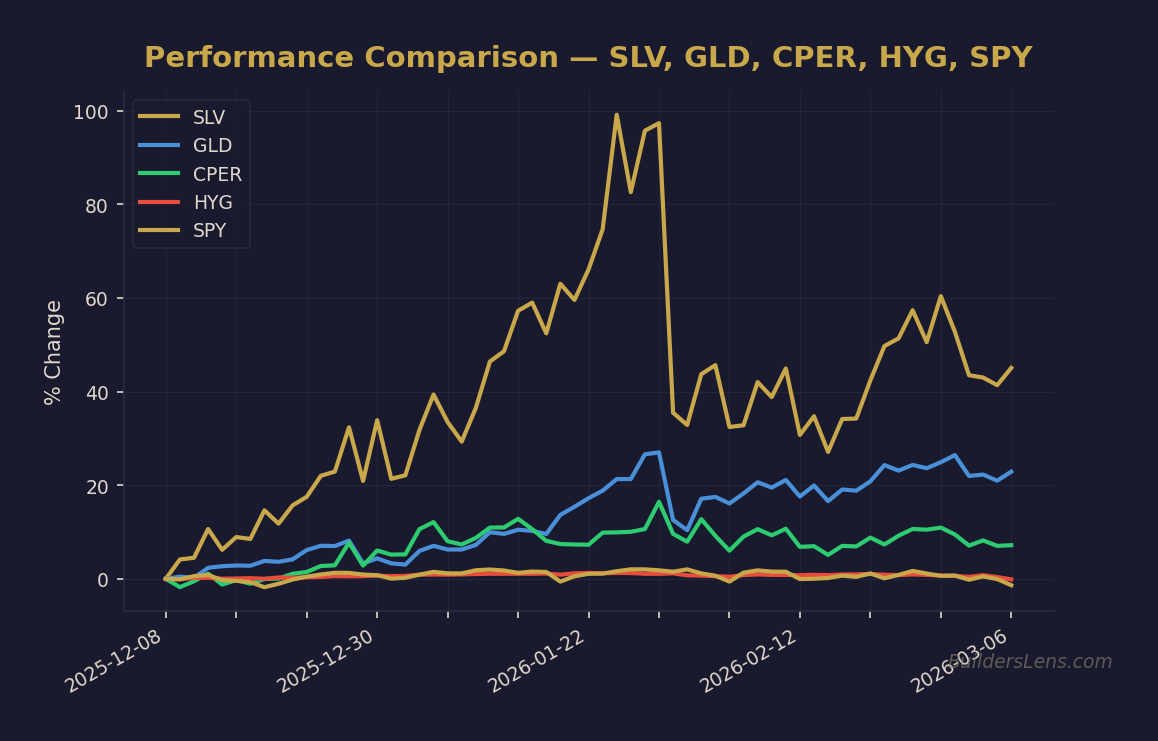

Silver’s rally was not powered by accelerating end-demand. It was driven by difficulty sourcing supply amid tariffs, logistics disruptions, and speculative positioning. That combination is inherently fragile.

Higher prices pull forward supply. Hoarded metal re-enters the market. The original scarcity fades — often faster than expectations adjust.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

The Gold-to-Silver Ratio as a Reality Check

The gold-to-silver ratio compressed into the mid-40s, levels last seen during periods of strong industrial demand. Today, that demand backdrop is absent. China — the marginal driver of industrial metals — is decelerating, not re-accelerating.

Copper Confirms the Message

Copper followed a similar path. Tariff fears and supply disruptions pushed prices higher, but inventories are now rebuilding in London and Shanghai. Rising stockpiles are incompatible with claims of strong real-economy demand.

Gold Is Sending a Different Signal

Gold’s relative resilience matters. The copper-to-gold ratio remains near historic lows, a configuration historically associated with deflationary or risk-averse environments — not inflationary overheating.

Phase Mapping and Probabilities

We place this episode within late Phase 1. Speculative excess is being unwound beneath still-elevated asset prices. This does not yet confirm a Phase 2 forced-liquidity cascade.

- Phase 1 continuation (next 3–6 months): ~50–60%

- Phase 2 transition risk: ~25–35%

- Phase 3+ outcomes: lower probability without credit confirmation

What Changes — and What Does Not

What changes: We increase skepticism toward momentum-driven commodity rallies without demand confirmation. We rely more heavily on ratios and inventories.

What does not change: Real assets remain part of long-run hedging. Short-term volatility does not invalidate long-term scarcity narratives.

Signals We’re Watching Next

- Stabilization or further mean reversion in the gold-to-silver ratio

- Copper inventory trends across major exchanges

- China growth and credit impulse indicators

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.