Research · Macro Regime

The Currency Reset Nobody Sees Coming

The Mechanism Behind Currency Erosion

Currency transitions rarely begin with panic. They begin with arithmetic. When debt service compounds faster than economic output, policy flexibility narrows. Governments can raise taxes, compress spending, or increase monetary accommodation. Historically, accommodation becomes the politically tolerable path.

This does not imply immediate collapse. It implies sequencing. Our Strategy evaluates these pressures through a phased macro framework that prioritizes liquidity mechanics, credit transmission, and yield structure over narrative intensity.

Phase Classification: Where We Are Now

We currently classify the environment as late Phase One: Melt-Up with Structural Cracks. Equity indices can remain resilient while underlying purchasing power compresses. Volatility can stay muted even as debt service expands. Markets often discount instability late.

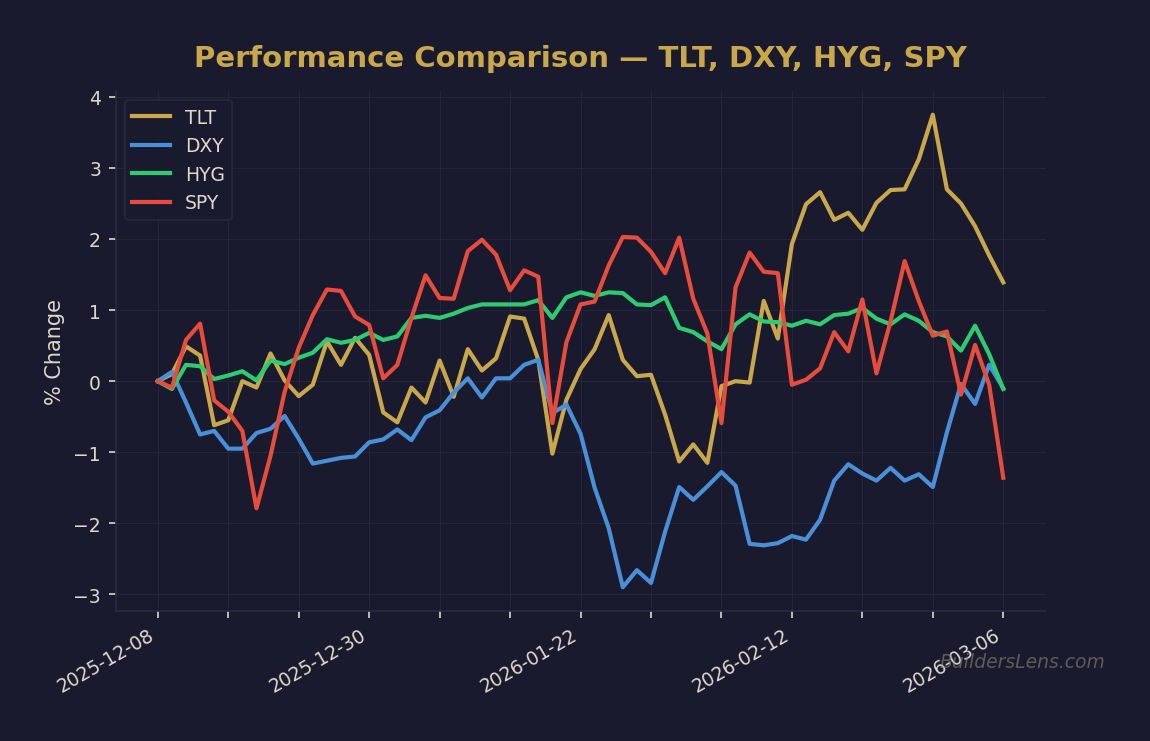

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Phase pressure increases when fiscal strain compounds alongside credit fragility and funding sensitivity. The key is not prediction. The key is monitoring transmission channels.

Date-Anchored Probability Timeline

Based on current signal alignment, Our Strategy assigns approximately:

- Sixty percent probability that late Phase One conditions persist through June 2026.

- Thirty percent probability that Phase Two forced-liquidity dynamics begin emerging before December 2026.

- Ten percent probability of extended melt-up conditions beyond mid-2026 without credit disruption.

If Phase Two materializes, the most probable transition window into Phase Three policy response would occur between December 2026 and June 2027.

What Would Confirm Acceleration

- Sustained credit spread widening.

- Funding market stress or weaker Treasury auction dynamics.

- Labor deterioration moving from noise into trend.

- Structural rollover in long-duration yields consistent with recession pricing.

What Would Invalidate Near-Term Reset Pressure

- Improving hiring rates and labor participation stabilization.

- Tightening credit spreads across high-yield and leveraged loans.

- Long-term yields compressing without renewed liquidity expansion.

That combination would extend melt-up dynamics and delay crash-cascade probability.

Multi-Asset Monitoring Framework

Our Strategy continuously monitors cross-asset confirmation:

- Rates: Ten-year and thirty-year yield direction, term premium sensitivity.

- Credit: High-yield spreads, private credit stress proxies.

- Liquidity: Repo dynamics, reserve conditions, auction tails.

- Dollar: DXY strength as global tightening mechanism.

- Market Internals: Breadth deterioration and volatility regime shifts.

What Changes — and What Does Not

What changes: concentration risk rises late-cycle, optionality becomes more valuable, and real asset leadership rotates gradually.

What does not change: disciplined sequencing, tranche-based deployment, and probability-based positioning remain core principles.

Currency degradation is rarely cinematic. It compounds quietly. The signal is not collapse. The signal is erosion.

Educational Disclosure

This content is for educational and informational purposes only. It reflects a probabilistic macro framework and does not constitute financial or investment advice.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze DXY (US Dollar Index)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.