Research · Macro Regime

The Monetary Shift Markets Haven’t Priced Yet

The Most Important Monetary Shift Since the End of the Gold Standard?

Markets often anchor regime change to visible crisis events. Two thousand eight. Twenty twenty. But structural monetary shifts rarely announce themselves through headlines. They emerge through funding mechanics, liquidity transmission channels, and subtle changes in global dollar demand.

Within Our Strategy framework, the question is not whether something dramatic is happening. The question is whether the plumbing beneath the system is tightening in a way that markets have not fully priced.

Framework Mapping: Where We Sit in the Phase Model

Under Our Strategy’s five-phase operational model, current conditions align most closely with late Phase One pressure, with rising drift toward Phase Two multiple compression.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

- Phase One continuation probability: Approximately sixty percent through mid twenty twenty six, assuming liquidity remains broadly supportive.

- Phase Two compression probability: Approximately thirty percent over the next several quarters if funding stress accelerates.

- Phase Three breakdown risk: Increasing into late twenty twenty six if credit spreads widen and liquidity momentum turns decisively negative.

This is not forecast language. It is sequencing language. Phase pressure rises or falls depending on signal alignment.

The Core Mechanism: Dollar Liquidity vs Global Debt

The structural issue is not simply policy rates. It is the interaction between global dollar demand and the supply of dollar liquidity.

If global debt remains elevated while long-duration yields stay structurally high, refinancing stress increases. That is the rollover constraint. Policy rates can decline, yet long yields remain firm due to term premium pressure and supply dynamics. That environment compresses multiples even without recession.

Markets often misread this phase because earnings can remain stable while valuation compresses beneath the surface.

Signal Stack Monitoring

Under Our Strategy signal hierarchy, the following conditions determine regime transition:

Labor Deterioration

Hiring rate declines, rising continuing claims, and broadening layoff trends would confirm economic transmission into credit risk.

Credit Stress

High yield spreads widening materially, private credit stress emerging publicly, and tightening lending standards would accelerate Phase Two pressure.

Yield Dynamics

Long-term yields remaining elevated despite slowing growth would reinforce rollover stress. A decisive yield rollover would activate duration sequencing.

Liquidity Plumbing

Weak Treasury auctions, repo stress, and visible funding strain would shift probabilities toward Phase Three.

Dollar Constraint

A structurally firm dollar tightens global conditions and pressures risk assets through funding channels.

What Changes vs What Does Not Change

What changes:

- Probability weight shifts toward multiple compression

- Duration sequencing becomes more relevant

- Liquidity momentum becomes primary driver over earnings narratives

What does not change:

- No all-in positioning

- Cash remains strategic optionality

- Sequence activation requires confirmation, not anticipation

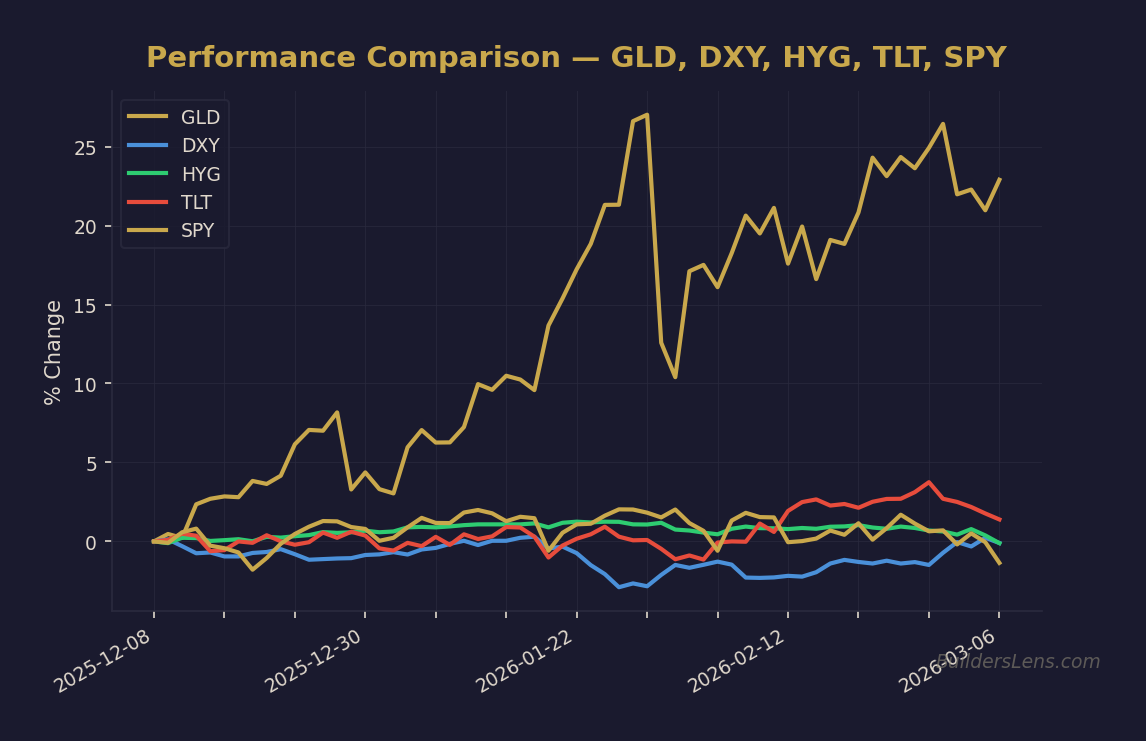

Monitoring Assets (Observation Only)

- SPY — broad equity beta

- TLT — first-duration layer

- ZROZ — convex duration layer, conditional only

- DXY — dollar constraint proxy

- High yield spreads — credit stress gauge

These are observation instruments, not trade signals.

Invalidation Conditions

This analysis would require reassessment if:

- Liquidity momentum reaccelerates materially

- Credit spreads remain compressed despite elevated yields

- Labor stabilizes with improving breadth

- Treasury auction demand strengthens consistently

Conclusion

The most important monetary developments rarely begin with dramatic declarations. They begin with subtle shifts in funding structure, term premium behavior, and global dollar flows.

Whether this period ultimately ranks alongside the end of the gold standard is less important than recognizing phase pressure in real time. Our focus remains on signal alignment, sequencing discipline, and probability weighting — not narrative conviction.

This content is for educational purposes only. It reflects a probability-based macro framework and does not constitute investment advice.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

→ Analyze HYG (High Yield Credit)