Research · Cycle Sequencing & Phases

The Payroll Revision That Rewrote the Cycle

Payroll Benchmark Revisions and Phase Recalibration

The recent benchmark revision reduced cumulative payroll gains by more than one million jobs relative to previously reported figures. This adjustment materially alters the perceived strength of the labor market dating back to late 2023 and requires recalibration of macro sequencing.

Our Strategy interprets benchmark revisions not as statistical anomalies but as delayed signal corrections. When employment growth is overstated, income growth appears stronger, consumer resilience appears firmer, and policy restraint appears justified. When revised lower, those assumptions must be re-evaluated.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Transmission Mechanism: Labor to Credit

The economic transmission pathway remains structurally consistent:

- Labor growth supports wage income expansion.

- Income growth supports consumption stability.

- Consumption sustains corporate revenue.

- Revenue stability sustains hiring and credit quality.

If hiring momentum was materially weaker beginning in late 2023, then the entire consumption and earnings narrative of 2024 must be reconsidered. Retail sales volatility and discount-driven surges are more consistent with thinner income growth than previously assumed.

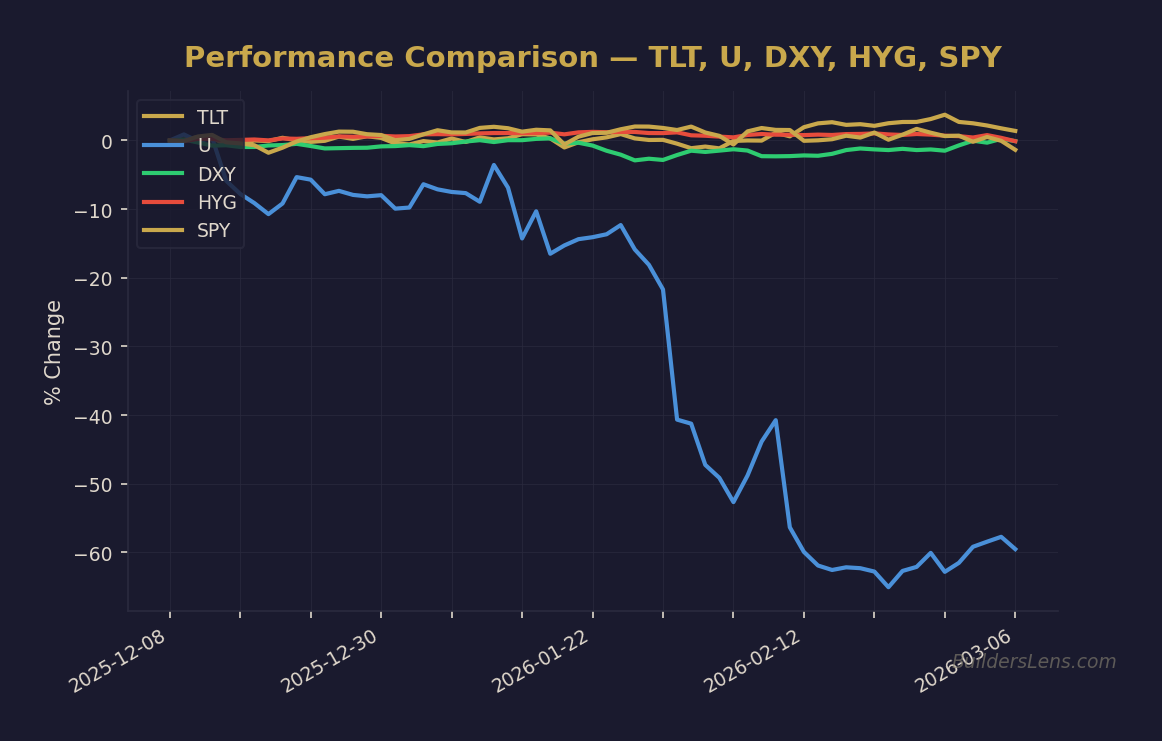

Rates Market Divergence

Long-term Treasury yields did not fully validate repeated claims of labor strength during 2024. That divergence suggests fixed income markets may have been discounting softer labor conditions earlier than equity narratives reflected.

In our framework, yield dynamics often signal sequencing shifts before equity sentiment adjusts. When rates refuse to confirm strength, structural deceleration probabilities rise.

Phase Mapping and Probability Calibration

Current Phase Assessment (Through June 2026)

We assign approximately a sixty five percent probability that the economy has been operating in a late-cycle deceleration regime since early 2024. This aligns with extended Phase One transitioning toward Phase Two within our operational framework.

Next Phase Risk Window (Late 2026)

We assign roughly a twenty five percent probability that labor weakness transmits more explicitly into credit conditions by late 2026 if income growth and hiring breadth continue to deteriorate.

Stabilization Scenario (Into 2027)

The stabilization path carries roughly a ten percent probability, contingent upon measurable reacceleration in hiring breadth, real income expansion, and sustained retail improvement.

Multi-Asset Monitoring Framework

- Rates: Ten-year Treasury yield, real yield trajectory, and term premium trends.

- Credit: High-yield spreads, lending standards, and default metrics.

- Liquidity: Treasury auction performance and funding stability indicators.

- Foreign Exchange: U.S. Dollar Index behavior as a tightening constraint.

- Equities: Breadth deterioration versus concentration resilience.

What Changes — and What Does Not

What Changes

- The credibility of single monthly payroll prints declines materially.

- Consumer pessimism appears more consistent with revised data.

- Bond market strength in late 2023 gains structural validation.

What Does Not Change

- Labor remains a lagging but decisive macro variable.

- Credit spreads remain the key transmission monitor.

- Liquidity plumbing and yield dynamics remain central to phase acceleration.

Invalidation Conditions

- Sustained improvement in hiring breadth through mid-2026.

- Broad-based real retail sales expansion beyond discount cycles.

- Credit spread compression alongside stable income growth.

If these conditions emerge, late-cycle deceleration probabilities decline materially and phase pressure recedes.

Conclusion: Sequencing Over Headlines

The payroll revision is not merely a historical correction. It is a recalibration of economic sequencing. Our Strategy emphasizes mechanisms over narratives and probabilities over conviction.

The interaction between labor, spending, credit, and yields will determine whether deceleration stabilizes or intensifies into late 2026 and 2027. Monitoring confirmation signals rather than reacting to isolated prints remains the disciplined approach.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze TLT (Long-Term Treasuries)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.