Research · Macro Regime

The ProSec Shift: Electricity, Security, and Market Risk

Production For Security: The New Steady State, The Risky Bridge

Our Strategy treats “production for security” as a macro regime transition, not a single trade. The destination may be stable: a world where nations accept higher costs in exchange for control over strategic inputs. The risk lives in the bridge between systems, where policy moves faster than infrastructure and where markets reprice both funding and feasibility.

The interview framing is blunt but useful: consumer goods can remain globally sourced, while strategic layers re-localize. No one cares where running shoes are made. They care where steel is made, where copper is smelted, where rare earths are processed, where chips are produced, and where electrons come from.

Our Strategy Framework: Mechanisms Over Narratives

Security-led production is best understood as an incentive redesign. Globalization rewarded efficiency. ProSec rewards controllability and redundancy. That means governments will increasingly tolerate what markets usually penalize: duplicate capacity, localized supply chains, and procurement rules that privilege domestic inputs.

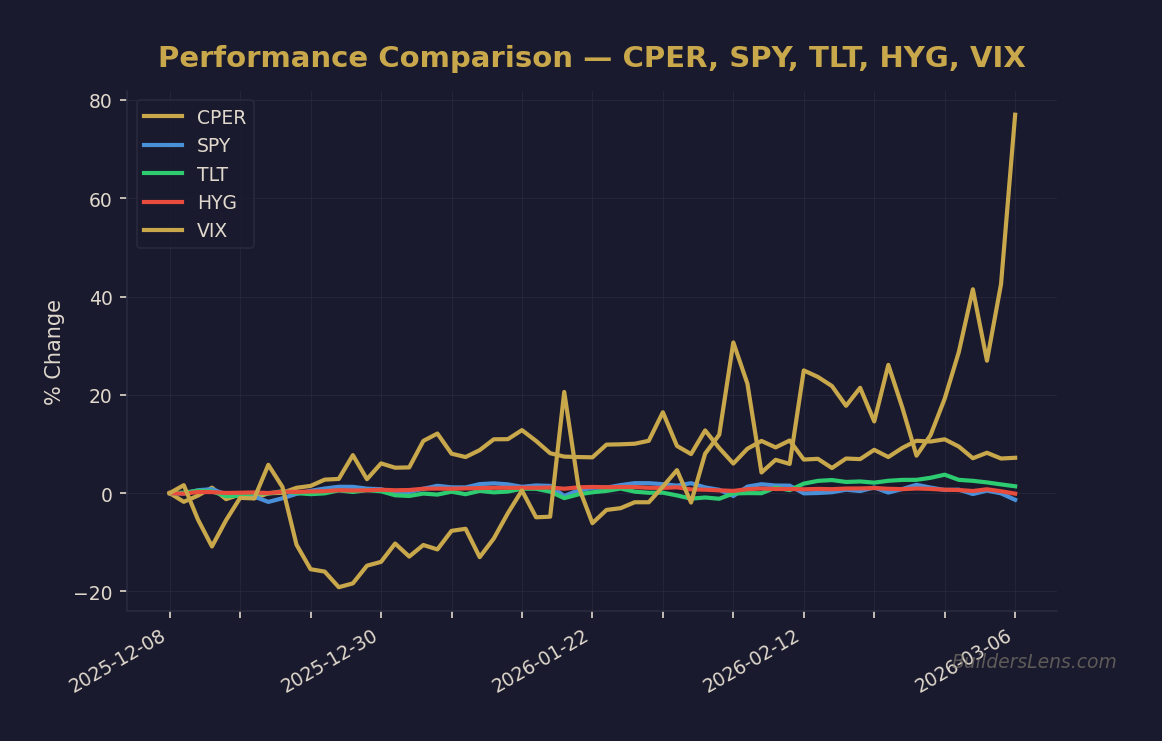

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

In other words, this is less about “spending more” and more about restructuring what qualifies as investable capacity. The same demand can produce very different outcomes depending on where bottlenecks sit.

The Real Constraint: Electricity, Not Just Defense Budgets

Our Strategy hears one dominant binding constraint across the entire ProSec stack: electricity. Data centers and artificial intelligence compute do not scale without power. Smelting and processing do not scale without power. Re-industrialization does not scale without power.

When power is abundant, ProSec behaves like a buildout story. When power is constrained, ProSec behaves like a rationing story. That is a major difference for margins, politics, and sequencing. It is also why household electricity bills can become a political variable, not just a utility line item.

Rare Earths: The Scarcity Is Processing and Refining

The most consistent misconception in public debate is that rare earths are scarce because they are rare. The scarcity is often downstream. Mining is only the start. Processing, refining, and industrial midstream capacity are the choke points, and those choke points are where security policy tends to land.

When governments realize that the dependency is not on the raw material but on the processed input, they move from symbolism to procurement. That is where “domestic content” requirements begin to matter as much as the commodity itself.

Policy As A Soft Price Floor Without Saying “Price Floor”

Our Strategy is careful with the phrase “price floor,” because administrations often dislike admitting they are creating one. But procurement can function like an implicit floor. If bids and contracts increasingly require domestic inputs or allied-sourced inputs, the demand becomes less price elastic and more policy anchored.

This matters because it changes the volatility profile. Policy-created demand can stabilize a sector over time, but the path there is rarely smooth. Rule changes, permitting realities, and budget politics can produce sharp repricings even when the long-run direction is intact.

Phase Mapping: Why The Theme Can Be Right And Still Whipsaw

Our Strategy frames ProSec inside cycle sequencing. Late Phase One can look resilient at the index level while internal dispersion rises. That is the environment where thematic trades can surge, then reverse, then surge again, because liquidity conditions and positioning dominate price action.

Phase Two pressure typically shows up as margin compression, leadership rotation, and widening dispersion between winners and losers. In that setting, the market is less forgiving of high valuation, high margin narratives, and more willing to reward tangible capacity, cash flows, and balance sheet strength.

Date-Anchored Probabilities: A Path, Not A Prediction

Our Strategy uses probabilities to keep optionality intact:

- Through June twenty twenty six: roughly sixty percent probability of remaining in late Phase One, with rising Phase Two pressure under the surface.

- By December twenty twenty six: roughly thirty percent probability of a deeper compression regime if labor weakens and credit spreads widen while long yields stay sticky.

- Through June twenty twenty seven: roughly twenty percent probability of a forced-liquidity phase if refinancing stress and funding conditions deteriorate materially.

These numbers are not a forecast. They are a structured way to express conditional sequencing.

What To Watch: Confirmations Versus Invalidations

Confirmations (Phase Two Pressure Rising)

- Persistent electricity price sensitivity and more grid and permitting friction.

- Widening credit dispersion beneath stable headline indexes.

- Procurement rules that explicitly favor domestic or allied inputs.

- More evidence that data center buildouts collide with state-level constraints.

Invalidations (Pressure Easing)

- Sustained easing in long yields that unlocks refinancing and lowers capex friction.

- Credit spreads remain contained while market breadth improves materially.

- Affordability pressure recedes through income catching up, not just inflation slowing.

Practical Frame: How Our Strategy Holds The Idea

We separate the destination from the path. The destination is a more security-oriented production system. The path is a multi-year transition constrained by power, permitting, capital, and politics.

So we do not treat ProSec as a single bet. We treat it as a regime backdrop that changes which bottlenecks matter, which margins compress, and which constraints become political.

Conversational Close

If you want our probability-based, phase-sequenced read of these transitions as they evolve, subscribe. The benefit is not a prediction. It is a repeatable way to interpret new information without being pulled into headline conviction.

Educational note: This is informational content only and not investment advice.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

→ Analyze HYG (High Yield Credit)

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

→ Analyze HYG (High Yield Credit)

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.