Research · Cycle Sequencing & Phases

The Starter Home Isn’t Gone — It’s Being Reengineered

Starter Homes Did Not Disappear. The Cost Stack Removed Them.

Our Strategy does not treat housing as a sentiment story. We treat it as a constraint-driven system. The modern starter-home shortage is best understood through a binding cost stack: land, labor, materials, financing costs, and zoning rules that often prevent smaller lots and higher density from emerging at scale.

When affordability breaks, markets typically adjust through one of three paths: prices fall, incomes rise, or structure changes. In many U.S. metros, the dominant adjustment has been structure, not nominal price. That means smaller interior footprints, tighter spacing, product-mix shifts toward townhomes and condos, and payment-engineered formats such as attached accessory dwelling units and build-to-rent communities.

The Core Mechanism: Land As The Binding Constraint

Builders can reduce variable construction costs by shrinking square footage, simplifying finishes, and standardizing plans. But when land is expensive, the per-unit land burden often dominates the total cost. In that environment, shaving a few hundred square feet does not meaningfully restore affordability unless:

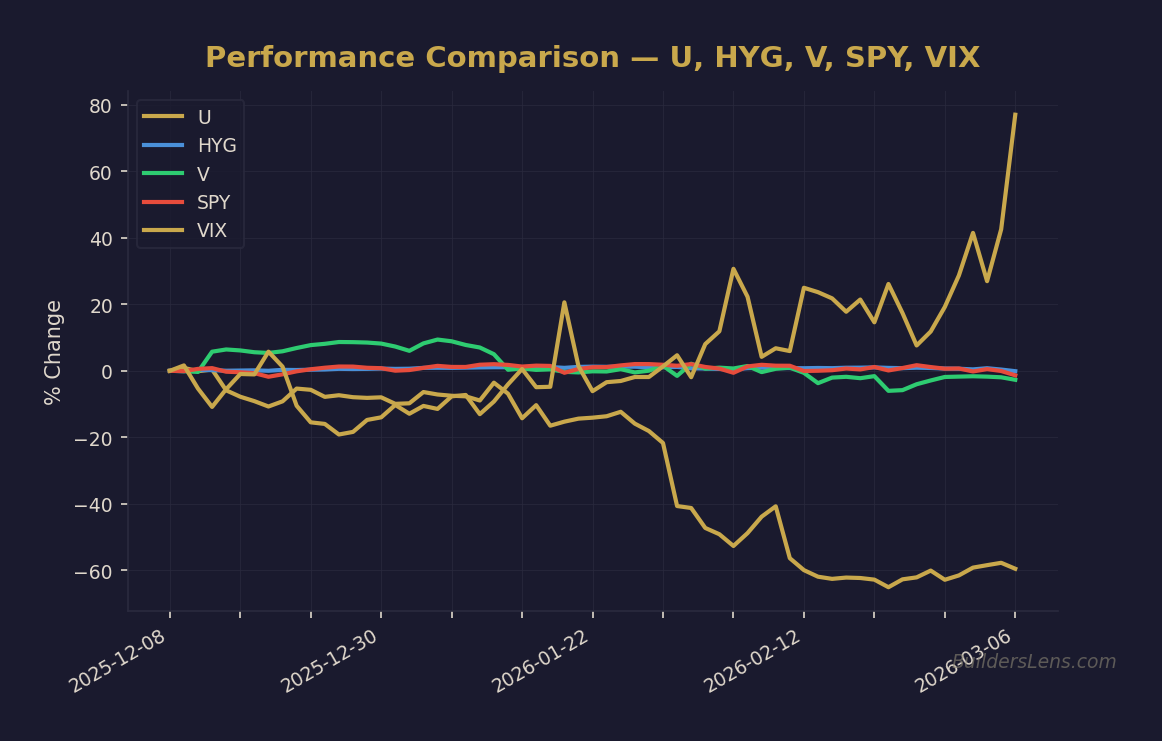

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

- buyers accept materially smaller homes at similar land burdens, or

- density rises so the land cost is shared across more units.

This is where zoning and parcel rules become central. If smaller lots are not permitted, or if neighborhood standards require larger minimum home sizes, builders are economically pushed toward maximizing revenue per lot. The system does not reward entry-level optimization when land remains the primary constraint.

Affordable Price Versus Affordable Payment

Our Strategy separates “affordable housing” from “affordable monthly payment.” These are structurally different solutions.

Attached ADUs and separate-entrance layouts are increasingly marketed as affordability tools. Mechanically, they function as household-level subsidy structures: the headline price remains similar, but the buyer attempts to offset the mortgage with rental income.

This is not inherently positive or negative. It is a transfer of risk. The developer and lender clear the transaction at a price that supports the land and construction stack. The household absorbs occupancy risk, rent volatility, and management friction. In stable environments, this can work efficiently. In stressed environments, it can amplify fragility.

Build To Rent: Structural Substitution

Build-to-rent communities represent another adaptation. The system is effectively offering the experience of a detached home without requiring mortgage qualification at prevailing rates.

From a phase perspective, substitution from ownership to rental formats — while headline prices remain firm — is consistent with late-cycle affordability pressure. This does not imply imminent collapse. It signals that the system is clearing through composition shifts rather than nominal resets.

Framework Mapping: Phase Sequencing, Not Prediction

Under Our Strategy’s probability-based framework, current housing dynamics align with late Phase One with rising Phase Two pressure. The system remains functional, but it is solving constraints through incentives and structural redesign rather than organic affordability.

Date-Anchored Probability Structure

- Continuation of late Phase One through mid 2026: approximately sixty percent probability, conditional on stable credit and labor conditions.

- Transition toward Phase Two compression between mid 2026 and year-end 2026: approximately thirty-five percent probability, rising if unemployment trends higher and credit spreads widen.

- Deeper Phase Three stress into 2027: lower probability scenario, conditional on systemic refinancing stress or funding disruption.

These are not forecasts. They are sequencing tools designed to manage uncertainty and avoid narrative conviction.

Signals We Monitor

Confirmations of Rising Phase Pressure

- Widening credit spreads, particularly in high yield and mortgage-backed securities.

- Rising unemployment and sustained increases in continuing claims.

- Escalating builder incentives and rising cancellation rates.

- Acceleration in condo, townhome, and build-to-rent supply relative to detached homes.

Invalidations

- Durable decline in long-term mortgage rates alongside stable real wage growth.

- Broad zoning reform enabling smaller lots and higher density at scale.

- Contained credit conditions with stable labor markets.

Investor Implications: Buy Toward Affordability

From an investor standpoint, affordability remains the anchor. Two-bedroom, two-bath formats often generate comparable rent to larger three-bedroom homes while requiring materially lower acquisition cost. In constrained wage environments, rent caps become binding at the high end.

Buying toward affordability aligns exposure with the broadest segment of demand. In late-cycle environments, that positioning historically demonstrates greater resilience than premium product exposure.

Closing Observation

The starter home is not extinct. It is being redesigned. Smaller footprints, denser layouts, ADU configurations, and rental substitutions are the market’s way of adapting to a constrained cost stack.

Our role is not to predict with certainty. It is to observe structural shifts, assign probabilities, monitor confirmation signals, and adjust as conditions evolve.

BuildersLens Research Hub: https://builderslens.com

Supported by V6D: https://v6d.com

Educational notice: This content is for informational purposes only and is not financial, investment, legal, or tax advice.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.