Research · Credit & Liquidity

The Truth About Seven Hundred Fifty Million in Debt

Debt Size vs. Debt Structure: A Phase-Based Analysis

Large debt figures trigger emotional reactions. Within Our Strategy’s probability-based framework, however, the relevant variable is not the size of leverage, but its structure, funding alignment, and survivability across liquidity regimes.

Productive leverage exists when debt is tied to income-generating assets with durable cash flow and fixed funding. Destabilizing leverage emerges when debt is attached to depreciating assets, floating-rate exposure, clustered maturities, or optimistic pro forma assumptions.

Mechanism: Cash Flow as the Transmission Channel

In the real estate structure discussed, equity capital is raised, construction financing is layered, the asset stabilizes, and refinancing returns capital without asset liquidation. The transmission mechanism is simple: tenant cash flow services the debt.

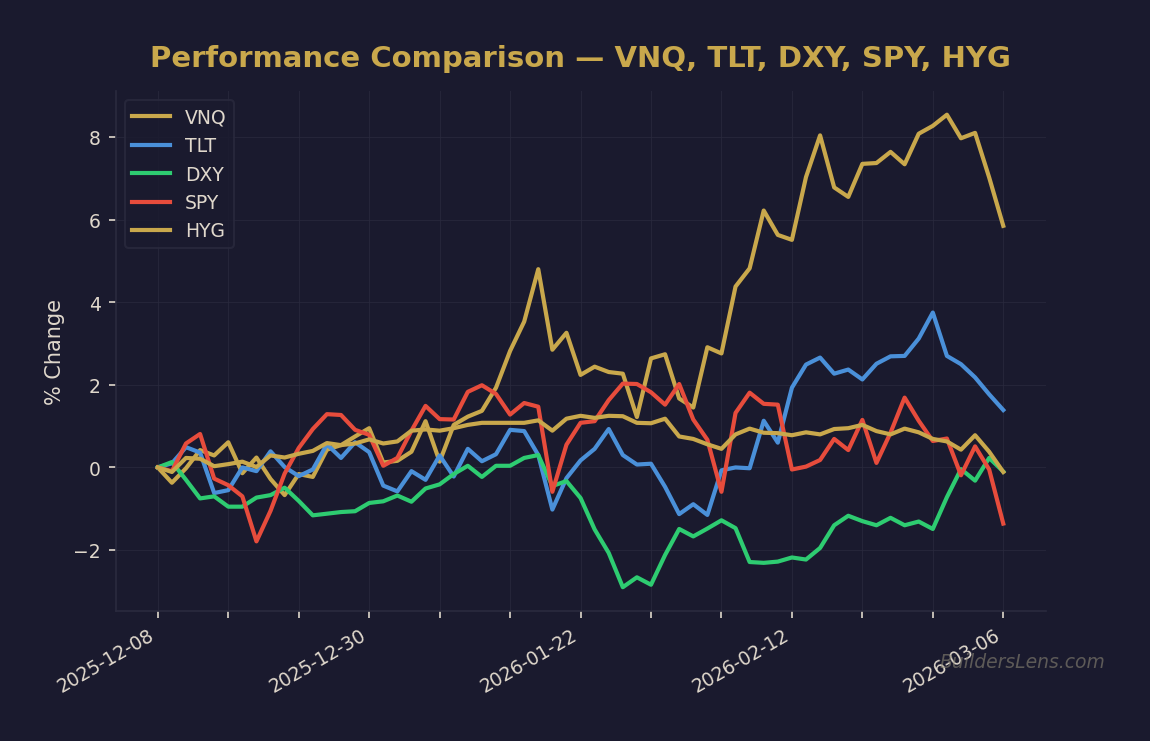

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

This structure can scale efficiently during stable liquidity conditions. However, durability depends on refinancing windows, term premium behavior, and credit availability.

Framework Mapping: Phase Alignment

- Phase One – Melt-Up / Liquidity Supportive: Structured, fixed-rate leverage compounds effectively.

- Phase Two – Multiple Compression: Floating exposure begins to tighten as funding costs reprice.

- Phase Three – Credit Stress: Refinancing risk accelerates. Coverage compression becomes visible.

- Phase Four – Forced Liquidity: Margin unwinds and distressed pricing emerge.

- Phase Five – Stabilization: Credit spreads normalize and disciplined leverage regains durability.

Date-Anchored Probability Bands

Through June 2026: Approximately 60% probability that well-structured, fixed-rate, cash-flowing leverage remains serviceable under stable liquidity.

Late 2026: Roughly 40% probability that refinancing stress rises if labor deterioration and credit tightening accelerate.

Into June 2027: Conditional probability of Phase Three or Phase Four depends on sustained spread widening and funding market strain.

Multi-Asset Monitoring Dashboard

- High-yield credit spreads

- Private credit default trends

- Long-duration Treasury behavior (TLT and ZROZ as observation proxies)

- Dollar strength (DXY)

- Equity breadth metrics (SPY, SMH as structural indicators)

What Changes vs. What Does Not

What Does Not Change: Debt remains a scalable tool when tied to durable cash flow and fixed funding structures.

What Changes: Floating-rate exposure, compressed debt service coverage, refinancing concentration, and tightening credit conditions can shift leverage from productive to destabilizing.

Invalidation Conditions

- Sustained tightening of credit spreads

- Stable refinancing windows with improving lending standards

- Improving labor market momentum

If these persist, downside phase pressure diminishes and structured leverage durability extends.

Conclusion

Debt is neither inherently dangerous nor inherently beneficial. Its impact depends on structure, liquidity alignment, and macro phase sequencing. Our Strategy evaluates leverage not by headline magnitude, but by mechanism, funding resilience, and probability of transition across regimes.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze DXY (US Dollar Index)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.