Research · Cycle Sequencing & Phases

Wage Growth Is Slowing — Housing Phase 2 Pressure Is Building

Housing Is Slowing — But What Phase Are We Actually In?

Wage growth is rolling over. Buyer demand is soft. Affordability remains stretched relative to income. The surface narrative suggests housing is “breaking.” Our Strategy asks a different question: where does this fit in the five-phase cycle?

Strategy Anchor

In Our Strategy, we operate inside a five-phase macro framework. We are not predicting headlines. We are tracking signals, sequencing, and transmission mechanisms. Housing is not evaluated emotionally — it is evaluated mechanically.

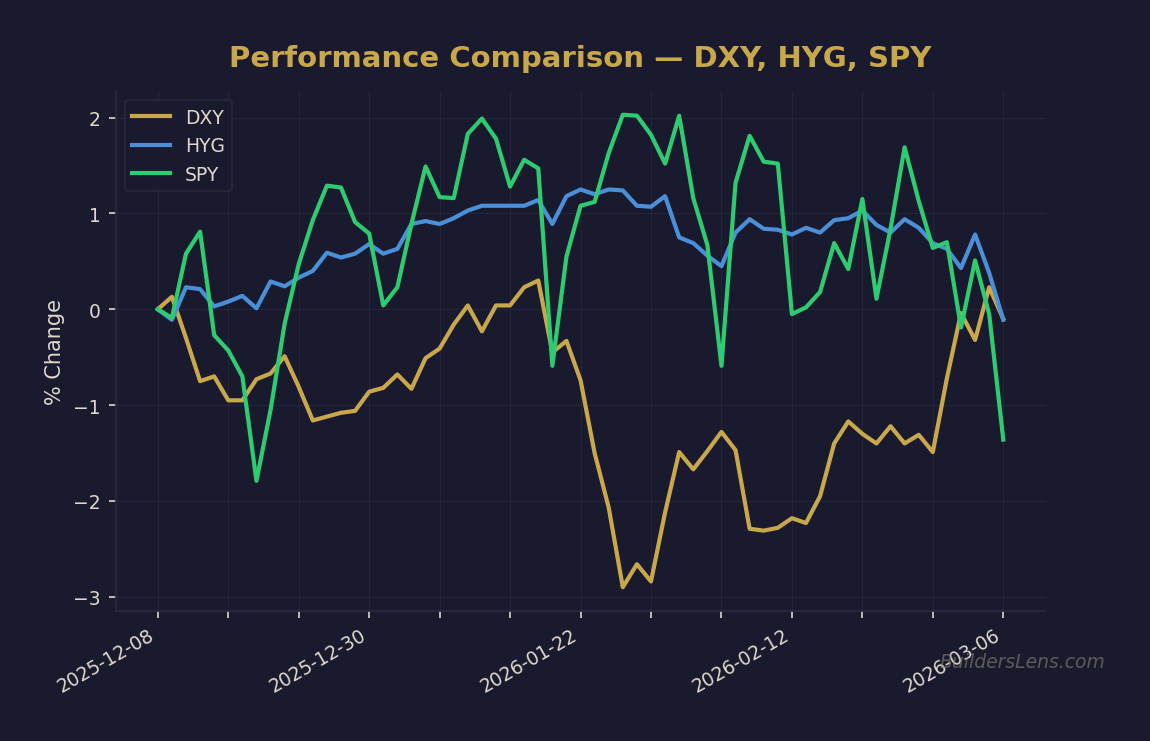

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

The key issue is not whether prices fall tomorrow. The key issue is whether slowing labor momentum increases Phase Two compression probability and eventually raises Phase Three credit stress risk.

What Actually Changed

The video highlights several measurable developments:

- Wage growth has slowed to multi-year lows.

- Pending sales remain weak year over year.

- Home tour activity has declined.

- The income required to qualify for a typical mortgage exceeds median household income in many metros.

These are labor and affordability signals. They are not yet credit stress signals.

The Mechanism: Why Labor Drives Housing

The transmission path is straightforward:

- Wage growth slows.

- Mortgage qualification slows.

- Transaction volume declines.

- Price discovery lags volume deterioration.

- If prolonged, credit stress emerges.

Housing weakness typically begins quietly through falling volume. Prices often adjust later. Markets can ignore this early stage because liquidity conditions elsewhere may still support risk assets.

Phase Mapping: Where This Fits

This housing signal reinforces late Phase One moving toward Phase Two pressure.

- Phase One: Liquidity supportive, melt-up participation.

- Phase Two: Multiple compression, rotation, valuation pressure.

- Phase Three: Credit stress and disorderly repricing.

At present, housing supports rising Phase Two probability. It does not confirm Phase Three.

Probability Timeline

Next 3 Months:

- 40–55% melt-up continuation

- 30–40% compression regime

- 10–20% disorderly stress

Next 6 Months:

- 35–45% Phase Two dominant

- 15–25% Phase Three emergence

- 30–45% extended late-cycle melt-up

Next 12 Months:

- 40–50% sustained Phase Two regime

- 25–35% credit stress window

- 20–30% continued melt-up extension

What Would Escalate This

- Rising mortgage delinquencies

- Widening high-yield spreads

- Tightening lending standards

- Dollar funding stress

Housing alone rarely triggers systemic breakdown. Credit transmission determines escalation speed.

What Changes in Our Strategy

- Tighter exit discipline on high-beta exposures.

- Increased monitoring of labor momentum.

- Heightened attention to mortgage delinquency data.

- Maintaining cash optionality.

What Does Not Change

- We do not front-run crash ladders without credit confirmation.

- We do not abandon melt-up participation if liquidity remains supportive.

- We do not treat anecdotal metro data as systemic evidence.

- We remain tranche-based and confirmation-driven.

Signal Dashboard to Watch

- Three-month annualized wage growth

- Mortgage rate direction relative to income

- Mortgage delinquency trends

- High-yield credit spreads

- Dollar index behavior

Sequencing matters more than headlines. Volume deterioration is early-stage pressure. Credit stress is the acceleration phase.

Final Framing

Affordability pressure increases Phase Two probability. It does not guarantee Phase Three. Housing is a slow transmission channel — until it is not.

In Our Strategy, we do not need to be early. We just cannot afford to be late.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.