Research · Cycle Sequencing & Phases

Walmart’s “Hiring Recession” Signal: When Household Buffers Run Thin

Walmart’s “Hiring Recession” Signal and the Household Constraint

When the world’s largest retailer openly references a hiring recession, we do not interpret that as a headline recession call. We interpret it as a mechanism disclosure. Our Strategy focuses on sequencing and probability, not labels.

The mechanism being flagged is straightforward: labor quality weakens, income growth stalls, household buffers thin, and behavior shifts. That shift does not require panic. It only requires the margin of error to disappear.

Mechanism First: How the Pressure Builds

Step One: Labor Softening Beneath the Surface

Hiring slows. Hours flatten. Real income excluding transfer receipts stagnates or turns negative. These do not always show up immediately in unemployment headlines, but they reduce the durability of household cash flow.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Step Two: The Bridge Phase

Consumers respond by increasing credit usage and drawing down savings. Spending can remain resilient during this bridge period, which often creates the illusion of economic stability.

Step Three: The Pivot

Once buffers thin and delinquencies rise, the pivot begins. Households shift from discretionary spending to debt repair and savings prioritization. That pivot is what retailers and consumer staples firms begin to see first.

Framework Mapping: Where We Are in the Five Phases

Phase One: Melt-Up With Cracks

Markets can appear resilient. Higher income spending can mask underlying weakness. Trade-down behavior can temporarily benefit discount retailers.

Phase Two: Multiple Compression and Rotation

As income quality deteriorates and consumer stress rises, valuation pressure increases. Leadership narrows. Risk appetite becomes more selective.

Phase Three: Credit Stress

If labor softening and delinquency acceleration align, credit becomes the transmission channel. Spreads widen. Refinancing conditions tighten. Liquidity sensitivity increases.

Phase Four: Forced Liquidity

This phase requires a funding constraint layered on top of deteriorating cash flow. It is conditional, not inevitable, and probability-based rather than calendar-based.

Date-Anchored Probability View (As of March 2026)

- Phase One into Early Phase Two Blend: Approximately 55 percent probability of persisting through mid-2026.

- Phase Two Dominant: Roughly 60 percent probability if labor weakness and income stagnation continue.

- Phase Three Credit Stress by Year End: Approximately 35 percent probability if delinquencies rise alongside labor softening.

- Phase Four Forced Liquidity Beyond: Lower but meaningful probability, conditional on tightening funding conditions.

These are conditional probabilities, not forecasts. They evolve with confirmations and invalidations.

Confirmations vs. Invalidations

Confirmations

- Continued weakness in hiring rates and hours worked.

- Real income excluding transfer receipts remaining flat to negative.

- Rising delinquencies across consumer credit categories.

- Persistent cautious guidance from consumer-facing firms.

Invalidations

- Sustained improvement in hiring and hours over multiple months.

- Real income growth outpacing inflation pressures.

- Stabilization and improvement in delinquency trends.

- Rebuilding of household savings buffers.

Why This Matters

A hiring slowdown is not simply about employment counts. It is about income quality and household durability. When households pivot from spending to balance-sheet repair, the shift can accelerate quickly because it changes the flow of money through the entire system.

Our Strategy remains confirmation-driven. We do not anchor on narratives. We track labor, income, credit, and liquidity in sequence.

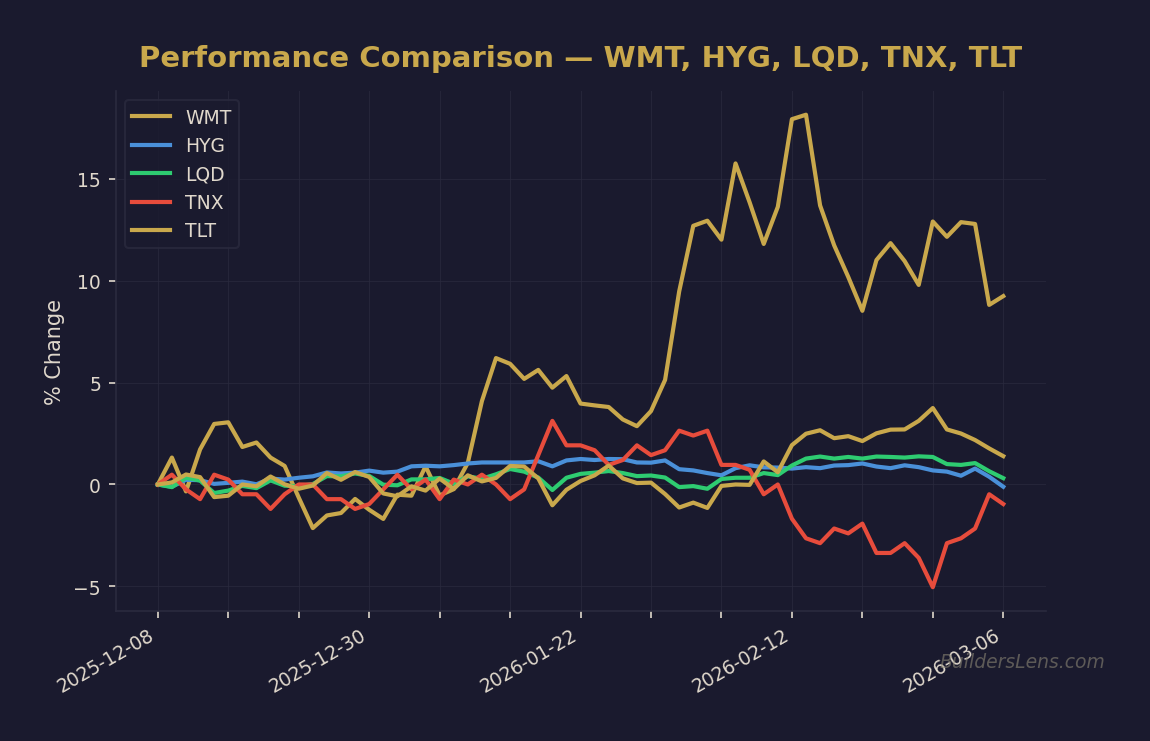

Monitoring Dashboard

- Consumer and Retail: WMT, XLY, XLP

- Credit Conditions: HYG, LQD

- Rates: 2-year, 10-year, and 30-year Treasury yields

- Risk Regime: SPY, VIX

- Dollar and Funding Signals: DXY and broad liquidity indicators

Educational Disclaimer

This content is for educational and informational purposes only. It is not financial, legal, or investment advice. All market decisions should be made based on individual objectives and risk tolerance.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

→ Analyze TLT (Long-Term Treasuries)

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.