Research · Narrative Translation

Wealth Is Built on Structure, Not Income

Money Is a Consequence, Not a Cause

Most people pursue money directly. Promotions, stock tips, speculative gains. Yet capital rarely compounds because it is chased. It compounds because structure supports it.

In Our Strategy, we analyze wealth through sequencing rather than motivation. Money is an output of alignment across debt, cash flow, time allocation, and system stability.

Debt as Negative Carry

High-interest consumer debt represents structural negative carry. Paying twenty percent while attempting to earn eight percent is not investing. It is erosion.

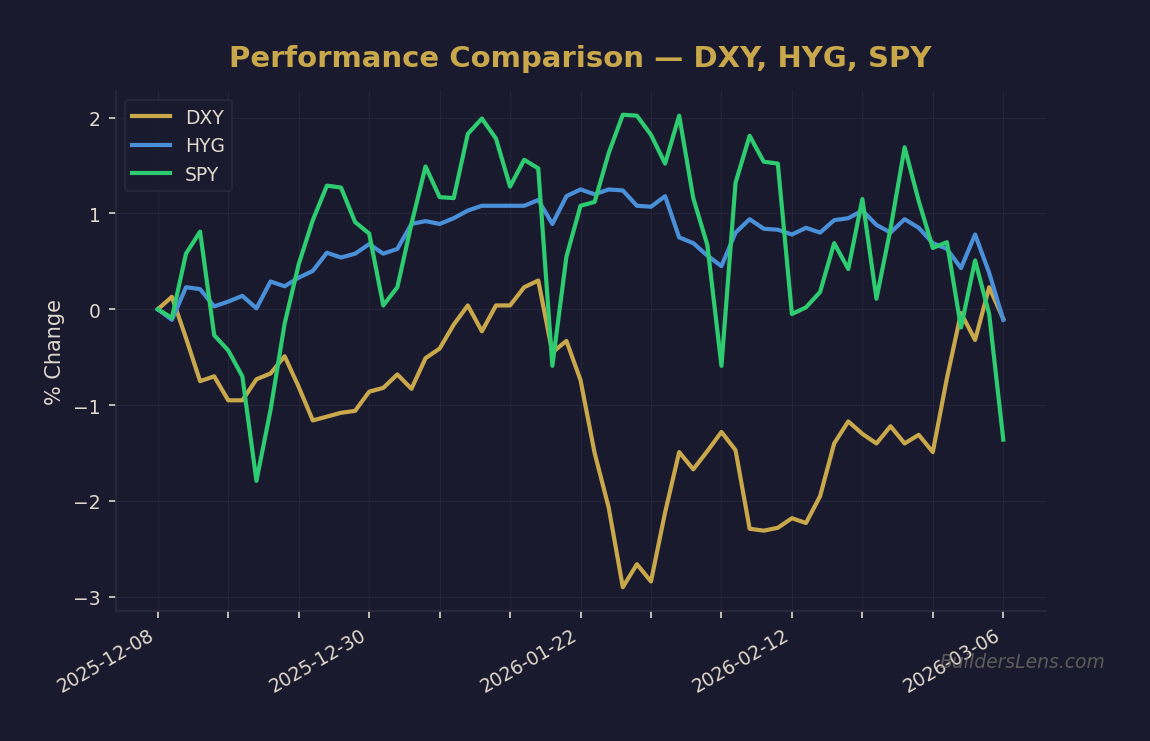

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

At the household level, this creates fragility. At the macro level, similar leverage imbalances precede credit stress.

As of early 2026, elevated consumer rates increase the probability that debt servicing constrains discretionary spending through mid-2026.

Cash Flow vs Appreciation

Appreciation requires liquidity expansion. Cash flow survives liquidity contraction.

During Phase 2 transitions, multiple compression erodes speculative assets first. Cash-flow-producing assets provide behavioral stability and optionality.

This distinction is structural, not philosophical.

2008 Through a Sequencing Lens

The 2008 crisis was mechanical deleveraging.

- Credit spreads widened.

- Liquidity froze.

- Forced selling accelerated.

Assets that continued producing income survived the freeze. Appreciation-only positions did not.

Rich vs Wealthy: Duration Matters

Short-duration capital seeks repeated transactions. Long-duration capital prioritizes survivability.

Wealth is optionality preserved across cycles.

Phase Probabilities

Through June 2026:

- Late-cycle churn remains the base case.

- Credit-stress acceleration remains possible but not dominant.

- Smooth normalization carries lower probability.

Into December 2026: Transition risk rises modestly if delinquency trends persist.

Into June 2027: Policy-response probability increases if leverage stress compounds.

What Changes vs What Does Not

What Changes

- Higher emphasis on cash-flow durability.

- Greater caution toward appreciation-only strategies.

- Maintained optionality into potential stress windows.

What Does Not

- No crash predictions.

- No timing precision claims.

- No abandonment of participation without confirmation.

Signals We Continue to Monitor

- Long yields relative to policy rates.

- Consumer delinquencies.

- Credit spreads.

- Housing liquidity.

- Dollar funding conditions.

Markets break when cash flow breaks. Sequencing determines survivability.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.