Research · Narrative Translation

When Commodities Become Strategic Assets: The Copper Signal

Why this copper interview matters in a macro framework

This episode is not primarily a call on copper prices. It is a discussion about sequencing and control: what changes when an industrial input begins to behave like a strategic resource. When governments start talking about strategic reserves, downstream processing capacity, and expedited permitting, the market is no longer only clearing on price. It is increasingly clearing on time, reliability, and political feasibility.

Our Strategy’s approach is mechanism-first. We do not need certainty about the next move. We need a clear view of what is driving the system so we can interpret signals in the correct order.

BuildersLens context synthesis

Recent BuildersLens work has emphasized a recurring pattern: markets can remain constructive on the surface while structural pressures build underneath. We treat this as late Phase One behavior with rising Phase Two pressure. In that environment, leadership can narrow, funding conditions matter more, and “story” assets often act as signals rather than mere outcomes.

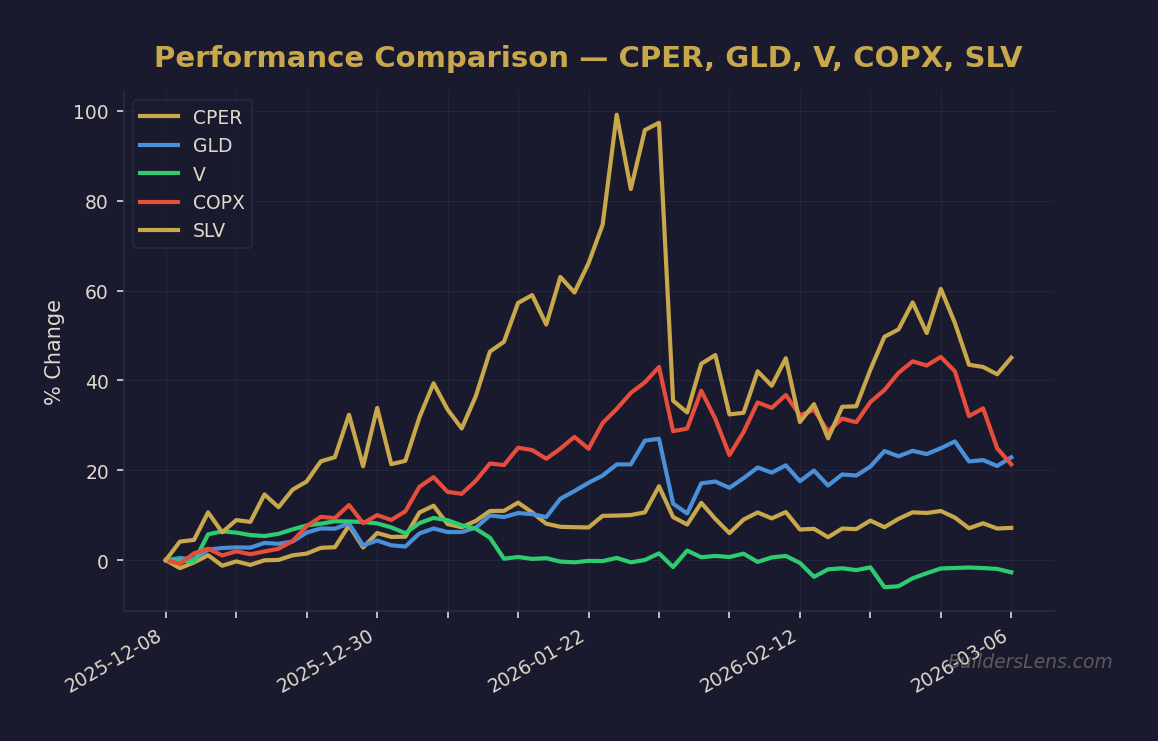

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

The copper conversation fits this lens because it centers on supply security, permitting speed, and midstream bottlenecks. These are structural variables that tend to matter more as regimes mature.

Mechanism one: strategic stockpiles change demand quality

Strategic reserves do not simply add demand. They change the type of demand. In normal cycles, buyers respond to price and inventory levels. In a strategic regime, buyers respond to security objectives, delivery timelines, and redundancy needs. That means demand can become less price-sensitive and more time-sensitive.

When that happens, the market’s transmission mechanism shifts. Price still matters, but it is no longer the only clearing variable. Policy becomes a buyer, and policy buyers tend to behave differently than purely commercial buyers.

Mechanism two: the supply chain bottleneck often lives in the middle

Copper does not move from mine to finished product in one step. The chain runs through concentrate, smelting, refining, and manufacturing. When constraints emerge, they often show up first in the midstream where processing capacity meets feedstock availability.

That is why midstream economics are informative. When processors compete for material, the bargaining relationship between miners and smelters can tighten. You do not need to forecast the next copper print to learn something from that. You watch for persistent signs that the system is operating closer to capacity, and that reliability is being repriced.

Mechanism three: capital intensity is the gating function for copper supply

Large copper projects are slow and expensive. The gating function is often not geology. It is the combination of capital intensity, permitting time, and cost of capital. This is why many promising projects remain stuck in long development timelines even during strong commodity tape.

In a strategic regime, governments may try to shorten that timeline through permitting prioritization and funding structures. But the market still requires a credible pathway to “yes.” Development is a sequencing problem: each milestone reduces uncertainty, and the value recognition often arrives in steps rather than a smooth curve.

Gold as a financing bridge to unlock copper

One of the most structurally interesting ideas in the discussion is the role of gold as a funding bridge. If a copper development project also contains meaningful gold revenue, it can widen the pool of available capital. Gold-linked financing structures and gold-oriented strategic partners can sometimes reduce the project’s vulnerability to a single funding window.

This does not mean a project is “safe.” It means it may have more optionality. In Our Strategy terms, optionality is valuable because it improves survival across regimes. When the environment shifts, the projects with multiple viable capital pathways are often the ones that keep moving.

How Our Strategy maps this to phase pressure

We frame this as late Phase One behavior with rising Phase Two pressure. That means markets can continue higher while internal stress quietly builds in funding, credit, and correlation behavior. Our goal is not to time a turn. Our goal is to keep the sequence of signals straight.

Here is our current probability map, expressed as regime odds rather than predictions.

- Phase One continuation: roughly sixty percent probability through June 2026, conditional on supportive liquidity and stable credit.

- Phase Two compression dominance: roughly forty percent probability by June 2026, conditional on liquidity momentum slowing and breadth deterioration.

- Phase Three credit stress: roughly thirty percent probability by December 2026, conditional on persistent spread widening and labor weakening confirmation.

- Phase Four forced liquidity window: roughly twenty percent probability by June 2027, conditional on clear funding stress, weaker auctions, and correlation spikes.

These probabilities are not additive. They are a discipline tool to keep us from turning a single narrative into a single outcome.

Mid–late video note: subscribe as a signal filter

If you want more of these mechanism-first breakdowns, consider subscribing. The benefit is simple: you get a consistent framework for separating signal from story, and for tracking confirmations and invalidations across regimes, rather than reacting to headlines in real time.

Quick educational disclaimer

This content is for educational and informational purposes only. It is not investment advice, and it is not a recommendation to buy or sell any asset.

What we would watch next

We separate confirmation signals from narrative noise. If copper is increasingly being treated as a strategic input, we expect to see real-world follow-through rather than one-off announcements.

Confirmations

- Policy execution: procurement frameworks, stockpile purchases, and funding programs that move from press release to implementation.

- Downstream build-out: evidence of permitting acceleration, processing incentives, and credible timelines for new capacity.

- Midstream tightness persistence: continuing indications that processing competition for feedstock remains elevated.

Invalidations

- Policy fade: security talk without procurement follow-through or tangible capacity progress.

- Regime stays risk-friendly: improving breadth, calm credit, and re-accelerating liquidity that keeps strategic metal narratives as background rather than a dominant driver.

- Constraint loosens: sustained evidence that bottlenecks are easing across the chain.

Disciplined takeaway

The strongest takeaway from this discussion is not “copper will do X.” It is that the system may be repricing reliability and security in real assets, and that policy can pull forward demand and compress timelines in ways that traditional cyclical narratives underweight.

Our Strategy stays focused on signals, sequencing, and probabilities. When an industrial metal becomes a strategic asset, the market’s structure can change. Our job is to watch for confirmation that the structure is changing, and to maintain optionality if it is.

Links

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer to see live macro positioning for tickers mentioned in this article:

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.