Research · Narrative Translation

When Crowded Trades Break: Bonds, Bitcoin, and Late Cycle Signals

Our Strategy translation: mechanisms over narratives

This episode with Jason Shapiro is useful because it separates crowding from direction, and forces us to treat market moves as delivery mechanisms: positioning, leverage, and liquidity.

In Our Strategy, “crowding” is not a signal to act by itself. Crowding is a pressure condition. It becomes actionable only when market behavior confirms that the crowded consensus is failing.

What the conversation is actually saying

Most of the dialogue can be translated into one idea: markets do not have to behave in extremes to be informative. The signal is often the opposite: when positioning is crowded and price refuses to validate the popular story, the market is quietly revealing where risk is mispriced.

Source: BuildersLens.com Signal Framework | Data as of March 08, 2026

Signal stack: Our Strategy map

- Positioning: where the crowd is leaning and how extreme it is

- Confirmation: whether price action validates or rejects the consensus

- Rates: long-end behavior, term premium pressure, auction tone

- Credit: spreads, refinancing stress, liquidity becoming a necessity

- FX: dollar constraint effects and funding sensitivity

- Leadership: rotation and breadth as regime texture

Crowded trade mechanics: sugar as a look-through

Shapiro flags heavy short positioning in sugar. Most viewers will dismiss it as niche, but our lens is mechanical: a crowded short can become unstable once price turns, because short covering is forced demand.

The value is not the commodity itself. The value is the potential transmission. Sugar links into ethanol sensitivity, and ethanol links into energy inputs. We do not need certainty on the chain. We only need to recognize that crowded corners can become pressure release valves.

Precious metals: when indicators miss, structure still speaks

Shapiro admits his positioning tools did not flag the metals move as crowded. Our takeaway is not to argue about the call. It is to treat synchronized violent moves across metals as a liquidity and leverage event first, rather than a clean retail sentiment story.

When multiple hard assets move together, we look for follow-through in rates and credit before calling it a regime shift.

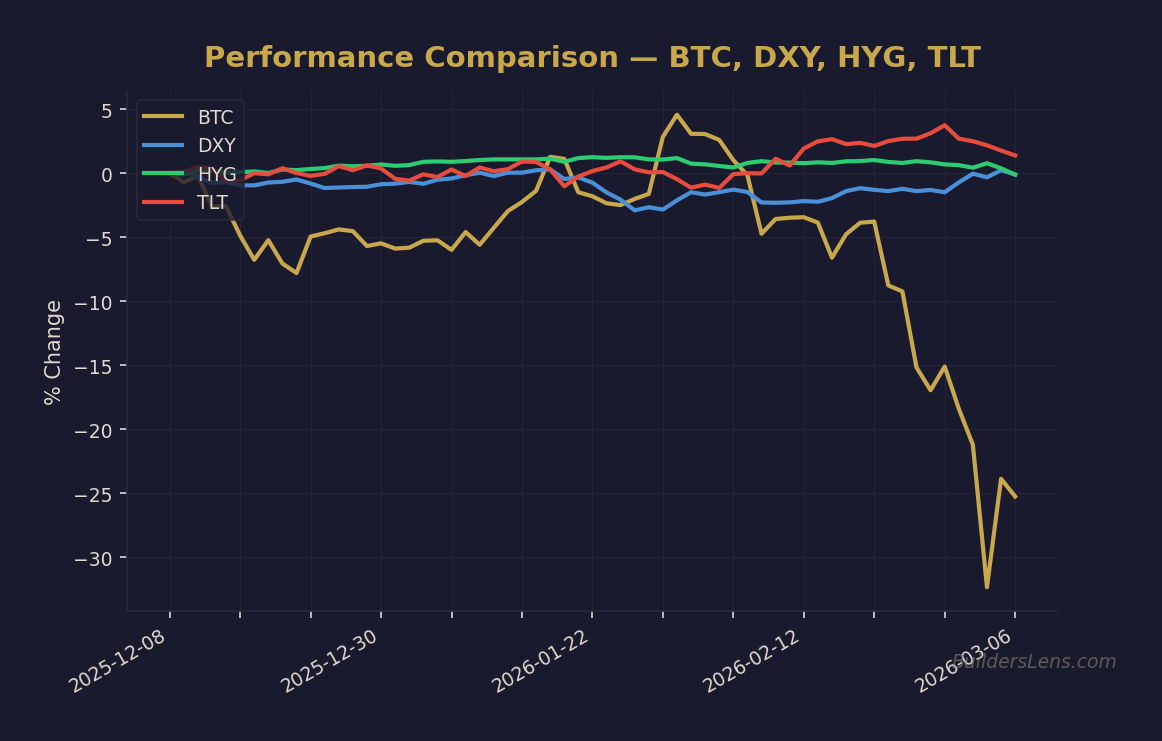

Bitcoin: rejecting the “million or zero” trap

The most useful framing in the conversation is that Bitcoin analysis often collapses into extremes. Our Strategy rejects that as a narrative trap. We treat Bitcoin as liquidity beta with convexity, not an ideological certainty.

Sentiment matters, but it is not a timing tool by itself. It becomes more informative when it aligns with the broader signal stack, especially dollar behavior, real yield shifts, and credit conditions.

Bonds: the market doing the opposite of the story

A key “weird” idea raised is the scale of short positioning in long duration exposure while bonds still behave resiliently. The narrative says deficits and borrowing should push yields higher. The signal is that price has not fully cooperated.

In Our Strategy terms, this is a signal over story moment. It does not guarantee direction. It tells us the consensus is crowded and the market may be setting up asymmetry if confirmation persists.

Yen carry trade: caution with stale causal models

The episode challenges the reflex claim that yen up equals carry unwind equals risk down. Our Strategy agrees with the warning: markets adapt, and the most popular causal chain is rarely the whole driver set late cycle.

FX narratives are treated as constraints, not single-cause engines. The dollar becomes most important when it appears alongside tightening credit and weaker funding signals.

Phase sequencing: probabilities, not conviction

Current phase: late Phase One, melt-up with cracks

Probability: roughly sixty to seventy percent through mid twenty twenty six, conditional on orderly funding and contained credit spreads.

Why: The discussion repeatedly returns to markets acting normal despite crowded narratives. That is consistent with late Phase One, where liquidity is present but reliability and leadership are shifting.

Next phase: Phase Two pressure rising, rotation and multiple compression

Probability: roughly twenty to thirty percent by December twenty twenty six if credit deterioration broadens and liquidity becomes more intermittent.

Why: Rotation into materials and energy, episodic volatility, and narrative fatigue can coexist with index resilience until funding becomes a necessity.

Plus one phase: Phase Three, credit stress becomes dominant

Probability: lower but non-zero by mid twenty twenty seven, conditional on widening spreads, refinancing stress, and weaker auction outcomes.

Confirmations and invalidations

Confirmations to watch

- Credit spreads widening with persistence, not one-off headlines

- Long-end yields rising through term premium with weaker auction quality

- Dollar strength coinciding with tighter funding conditions and weaker breadth

Invalidations to respect

- Credit spreads remain contained and refinancing channels stay open

- Auction demand stays orderly and yields stall or roll over without disorder

- Breadth stabilizes or improves even as leadership rotates

Sources and context

BuildersLens: https://builderslens.com

Sponsor: https://v6d.com

Disclosure

This article is for educational and informational purposes only. It reflects a probability-based analytical framework and is not financial advice, investment advice, or a recommendation to buy or sell any asset.

Get the Daily Phase Brief

Signal changes, data releases to watch, and today’s regime assessment — delivered every morning before market open.

Join investors tracking the macro cycle. Unsubscribe anytime.

📊 Run Your Own Analysis

Use the BuildersLens 65-Signal Analyzer for live macro positioning:

→ Analyze HYG (High Yield Credit)

→ Analyze TLT (Long-Term Treasuries)

This article is for educational and informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions.